10 Ways to Build Resilient Rental Properties

Jerry Chu

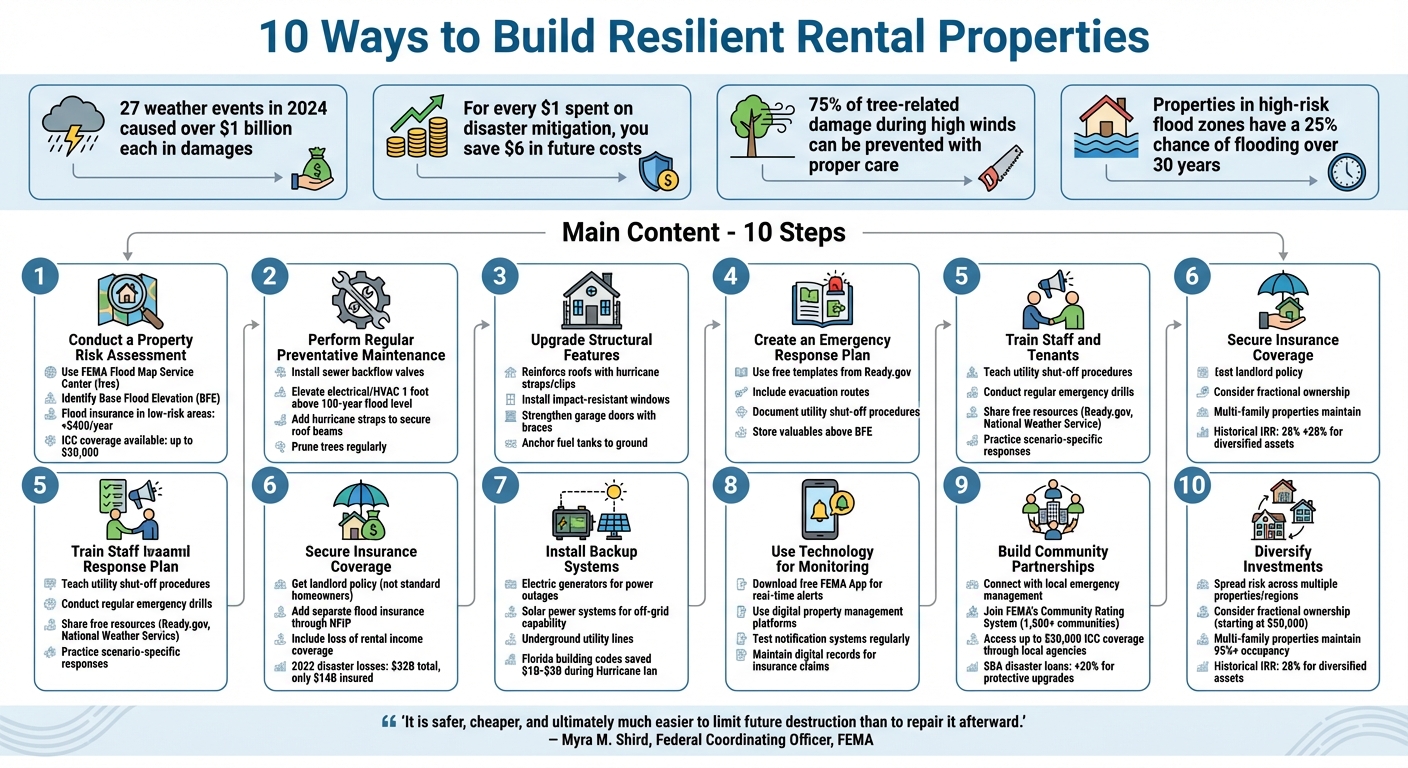

Natural disasters are becoming more frequent and costly, putting rental properties and tenants at risk. In 2024, the U.S. faced 27 weather events, each causing over $1 billion in damages. Protecting your rental property isn’t just about avoiding financial losses - it’s about ensuring tenant safety and maintaining steady income. For every $1 spent on disaster mitigation, you save $6 in future costs. Here's how you can safeguard your investment:

- Conduct a Property Risk Assessment: Identify vulnerabilities using FEMA tools and local experts.

- Perform Regular Maintenance: Prevent damage by addressing risks like tree hazards and water backups.

- Upgrade Structural Features: Reinforce roofs, windows, and utilities to withstand disasters.

- Create an Emergency Response Plan: Outline evacuation routes, utility shut-offs, and safety procedures.

- Train Staff and Tenants: Ensure everyone knows how to act during emergencies.

- Secure Insurance Coverage: Invest in landlord policies, flood insurance, and loss-of-income protection.

- Install Backup Systems: Use generators, solar power, and sewer backflow valves for added security.

- Use Technology: Leverage apps for real-time alerts and digital tools for property monitoring.

- Build Community Partnerships: Work with local agencies to access funding and expertise.

- Diversify Investments: Spread risk by investing in properties across different regions.

These steps not only protect your property but also reduce downtime, improve tenant retention, and ensure long-term stability. The key is preparation - start today to secure your rental property against future disasters.

10 Essential Steps to Build Disaster-Resilient Rental Properties

Energy Efficient & Disaster Resilient Homes | Robert Klob on Real Estate Investing Pros Show”

sbb-itb-a24235f

1. Conduct a Property Risk Assessment

Before diving into property upgrades, it's crucial to evaluate the specific risks your property might face. A detailed risk assessment helps pinpoint vulnerabilities tied to your location and directs you toward the most effective safety measures. Using government resources and local expertise can provide valuable insights to guide your decisions.

Start by using the FEMA Flood Map Service Center to check your property's flood zone designation. Then, identify the Base Flood Elevation (BFE) - the water level expected during a 100-year flood. This is key for determining how high utilities and other critical systems should be elevated. Properties in high-risk zones carry a 25% chance of flooding over 30 years, while those in low-to-moderate risk areas are five times more likely to experience flooding than a fire during the same period.

But don't just focus on flood risks. Examine structural vulnerabilities, like your roof's resistance to uplift, the wind load capacity of doors, and the impact resistance of windows. Also, ensure mature trees are planted at a distance greater than their full height to minimize storm-related damage. For a more localized perspective, consult with floodplain and emergency managers, who can offer insights into specific wind and water hazards that might not be reflected in online maps.

Cost of Implementation

The good news? The initial costs for this assessment are minimal. FEMA's online tools are free, and many local building departments or floodplain managers provide consultations at no charge. If you need a professional evaluation, licensed contractors can provide estimates tailored to your property's size and complexity. For properties in low-to-moderate risk areas, flood insurance can cost less than $400 annually. Additionally, eligible policyholders may qualify for up to $30,000 in Increased Cost of Compliance (ICC) coverage to help cover mitigation expenses after substantial damage.

With these low upfront costs, you'll gain the insights needed to improve tenant safety and secure your rental income from off-market properties.

Long-Term Benefits for Property Resilience

A well-executed risk assessment paves the way for smarter, targeted improvements. For example, elevating your property above the BFE can lead to lower flood insurance premiums. Plus, keeping essential systems operational during disasters ensures tenants can return home faster. By reducing downtime and vacancy periods, you'll not only protect your tenants but also safeguard your rental income.

2. Perform Regular Preventative Maintenance

Taking a proactive approach to property upkeep can help protect your rental property from the devastating effects of disasters. Regular maintenance not only safeguards your real estate investment but also minimizes the likelihood of severe losses. For example, an astonishing 75% of tree-related damage during high winds can be avoided with proper care.

"It is safer, cheaper, and ultimately much easier to limit future destruction than to repair it afterward." - Myra M. Shird, Federal Coordinating Officer, FEMA

Risk Mitigation Effectiveness

Routine maintenance lays the groundwork for protecting your property, but targeted measures can address specific disaster risks more effectively. For instance, installing sewer backflow valves can prevent expensive sewage backups. Elevating electrical boxes, HVAC systems, and major appliances at least one foot above the 100-year flood level ensures these critical systems stay functional during floods. Adding flood vents to foundation walls allows water to pass through safely, reducing the pressure that could otherwise damage your property’s structure.

When it comes to wind and storm preparation, the focus shifts to preventing debris from becoming hazardous projectiles. Reinforce garage doors with braces and strengthened glider tracks to protect these vulnerable entry points. Hurricane straps, which secure roof beams to walls, can help roofs withstand high winds. Pruning trees to eliminate weak or overhanging branches significantly reduces the risk of storm-related tree damage.

Cost of Implementation

Many preventative maintenance tasks can be folded into your existing property management routine without breaking the bank. Simple steps - such as securing outdoor furniture with anchors, cleaning gutters seasonally, and trimming trees - require minimal effort and cost but deliver meaningful protection. In flood-prone areas, replacing carpeting with tile during tenant turnovers adds a layer of flood resistance without a major financial commitment.

Some upgrades, like elevating HVAC units or installing backflow valves, may require professional contractors to meet code requirements. Fortunately, financial assistance is available. For example, the U.S. Small Business Administration provides disaster loans that can be increased by up to 20% to cover the cost of disaster-proofing projects. Additionally, elevating a property’s lowest floor above the Base Flood Elevation can lead to savings on flood insurance premiums.

Ease of Adoption for Property Owners

Wind-mitigation improvements can often be seamlessly integrated into routine maintenance. Low-cost upgrades - like installing heavy-duty deadbolts that penetrate deep into framing or using longer hinge screws on entry doors - can significantly boost wind resistance. Securing outdoor items such as fuel tanks, sheds, and trash cans with cables prevents them from turning into dangerous projectiles during storms.

Scheduling maintenance by season can make these tasks more manageable. For example, inspect and service water heaters and furnaces before winter, and clean gutters or check flood vents ahead of heavy rain seasons. Regular exterior inspections not only help you monitor the property’s condition but also provide photo documentation that can simplify insurance claims if disaster strikes.

Long-Term Benefits for Property Resilience

Consistent maintenance pays off over time, creating a ripple effect of benefits. After a disaster, quick actions like removing wet carpet and drywall can prevent secondary problems such as mold growth. Consulting with a local floodplain manager to confirm your property’s Base Flood Elevation ensures that elevation projects meet local standards. Combined with regular risk assessments, these maintenance efforts protect your property’s value and ensure tenant safety for years to come.

3. Upgrade Structural Features for Durability

Strengthening your property's structural features is a key step in boosting its resilience against severe weather. While routine maintenance addresses everyday wear and tear, targeted upgrades focus on fortifying critical systems like the roof, walls, foundation, and utilities. These changes can transform a property into one better equipped to handle hurricanes, floods, and other extreme conditions.

Risk Mitigation Effectiveness

Investing in structural reinforcements can significantly reduce damage during disasters. For example, elevating HVAC units, electrical panels, and major appliances at least one foot above the 100-year flood level can help prevent fire risks and equipment loss. Installing sewer backflow valves is another essential measure to block floodwaters from causing sewage backups. Anchoring fuel tanks securely to the ground can prevent them from floating or tipping, reducing the chance of spills and fires.

Wind resistance upgrades are equally critical. Adding hurricane straps or clips secures the roof to the walls, helping to prevent the roof from being torn off during high winds. Gable walls can be braced to rafters or joists to guard against collapse. For windows, options like storm shutters, shatter-resistant film, or high-impact glass can stop debris from breaching the building. Garage doors can also be strengthened with braces and reinforced tracks to handle intense wind pressure.

These measures not only protect the property but also offer peace of mind and economic advantages over time.

Cost of Implementation

Structural upgrades may seem expensive upfront, but the long-term savings make them a smart investment. Research shows that every $1 spent on disaster mitigation saves $6 in future damages. Plus, there are financial resources available to help offset costs. For instance, property owners with National Flood Insurance Program (NFIP) policies may qualify for up to $30,000 in Increased Cost of Compliance (ICC) coverage to meet mitigation requirements after significant damage. Similarly, U.S. Small Business Administration disaster loans can include up to a 20% increase specifically for protective upgrades.

To ensure your upgrades meet local codes and provide maximum protection, hire licensed contractors and consult with your local building department and floodplain manager. This will help you understand permit requirements and confirm your property's Base Flood Elevation (BFE). Beyond disaster protection, these improvements can lower flood and multi-peril insurance premiums, offering ongoing financial benefits.

Long-Term Benefits for Property Resilience

The benefits of structural upgrades extend well beyond their initial installation. Reinforced properties are often quicker to reoccupy after disasters, reducing downtime and lost rental income. Tenants also tend to feel more secure in buildings with visible protective features like impact-resistant windows or reinforced doors, which can help improve tenant retention.

The rebuilding phase after a disaster provides an ideal opportunity to implement these upgrades. FEMA's Federal Coordinating Officer Myra Shird emphasizes this point:

"The rebuilding phase of a disaster is the ideal time to consider ways to strengthen your home to protect people and property"

In addition to protecting against catastrophic damage, these upgrades help maintain property value and create a comprehensive defense system. Each improvement works together to safeguard both your investment and the well-being of its occupants. For those looking to invest in U.S. real estate with built-in diversification, tokenized models offer a modern alternative to traditional ownership.

4. Create an Emergency Response Plan

Once you've assessed risks and made structural updates, the next step is crafting an emergency response plan. This step is crucial for safeguarding your property and investment. To create a plan that addresses your property's unique risks, consult local floodplain and emergency managers. Their expertise helps you focus on real threats rather than generic scenarios.

Your emergency response plan should include essentials like an emergency kit, evacuation routes, and instructions for shutting off utilities. Keep important documents and valuables in waterproof containers stored above the Base Flood Elevation (BFE). If you're unsure where to start, Ready.gov offers free templates that guide you through the process, ensuring you cover all the critical elements. Taking the time to plan ahead can significantly reduce the impact of disasters.

Cost of Implementation

Creating an emergency plan is a budget-friendly task, requiring mostly your time and effort. With free templates available from Ready.gov, the planning process itself costs little. However, you may need to allocate funds for items like emergency supply kits, waterproof containers, and backup power solutions. While these initial expenses may seem like an extra burden, they are minimal compared to the potential financial toll of disaster recovery.

Long-Term Benefits for Property Resilience

A well-thought-out emergency response plan not only reduces the chaos during a disaster but also speeds up recovery. Properties with clear procedures recover faster because both owners and tenants know exactly what steps to take. This means less downtime, fewer interruptions to rental income, and a quicker return to normal operations.

Additionally, having a plan in place offers peace of mind. It reassures both property owners and tenants, fostering a sense of security that can boost tenant satisfaction and retention. To keep your plan effective, review it annually. During these reviews, check that your insurance coverage aligns with your community's specific risks, such as floods or high winds, as standard policies often exclude these hazards. Regular updates to your plan ensure you're always prepared, strengthening your property's resilience and enabling quicker recovery when it matters most.

5. Train Staff and Tenants on Emergency Procedures

An emergency plan is only as good as the people executing it. To turn plans into action, both staff and tenants must understand their roles when disaster strikes. As Nick Thornton, Head of Operational Resilience for Global Banking at J.P. Morgan, wisely states:

"You can't practice in the middle of an incident".

Start with the basics to prevent additional hazards. Teach everyone how to shut off gas, water, and power lines during earthquakes or storms to minimize the risk of fires or flooding. For specific emergencies, train for scenarios like earthquakes (“Drop, Cover, and Hold On”), wildfires (removing flammable items), and hurricanes (securing outdoor objects). These steps help bridge the gap between knowing the plan and putting it into action, making your emergency strategy more effective for those who buy tokenized real estate.

Cost of Implementation and Risk Mitigation Effectiveness

The good news? Implementing training doesn’t have to break the bank. Property owners can guide tenants to free resources like Ready.gov, the National Hurricane Center, and the National Weather Service for safety tips and plan templates. Share downloadable checklists, evacuation maps, and incorporate emergency protocols into the move-in process.

Regular drills are a must to test and refine your plan. Conduct fire drills, practice shutting off utilities, and test notification systems to ensure everyone knows their responsibilities. Encourage tenants to document property conditions before evacuations, which can speed up insurance claims later.

Long-Term Benefits for Property Resilience

Well-trained tenants can act quickly in emergencies. For example, they can remove wet materials after a flood to prevent mold and structural damage. This kind of proactive response not only reduces the severity of damage but also shortens recovery times, helping residents return home faster. Plus, properties with clear safety measures tend to attract and retain reliable tenants, offering peace of mind and a stronger sense of community.

6. Secure Insurance Coverage and Financial Reserves

Insurance is your safety net when disaster strikes. A standard homeowners policy won’t cut it for rental properties - you’ll need a landlord policy that includes property damage, liability, and coverage for lost rental income. Additionally, don’t overlook flood insurance. Even if your property is in a lower-risk zone, securing a separate flood policy through the NFIP or a private insurer can protect you from costly surprises.

Risk Mitigation Effectiveness

Natural disasters take a massive financial toll. In the first quarter of 2022, global disasters caused $32 billion in losses, but only $14 billion of that was insured. This gap left countless property owners scrambling to cover repair costs. Krista Reuther from TurboTenant puts it bluntly:

"The best time to insure your property was yesterday; the second best time is today. Don't wait until disaster strikes to evaluate your options - by then, it'll be too late."

Tailor your coverage to your property’s location. Coastal properties may need windstorm and hurricane policies, while earthquake-prone areas often require specific riders. For landlords, loss of rental income coverage is a game-changer, ensuring your cash flow doesn’t dry up if your property becomes uninhabitable. While these policies might seem expensive upfront, they’re a long-term investment in financial security.

Cost of Implementation

Comprehensive insurance does come with initial costs, but there are ways to ease the financial burden. For example, eligible NFIP policyholders may qualify for up to $30,000 in Increased Cost of Compliance (ICC) funds. Similarly, U.S. Small Business Administration (SBA) disaster loans can be increased by up to 20% to cover upgrades that make your property more disaster-resistant.

It’s also wise to set up an emergency fund to handle deductibles and minor repairs. Document your property’s current condition with photos and videos - this can make insurance claims much smoother. Finally, confirm that your policy covers replacement costs rather than actual cash value, which can leave you footing a larger bill.

Long-Term Benefits for Property Resilience

Proactive insurance and financial planning don’t just protect your property - they also reinforce tenant trust. Properties with robust coverage bounce back faster after disasters, reducing downtime and preserving tenant relationships. In 2024 alone, the U.S. faced 27 weather and climate disasters, each causing over $1 billion in damages. Landlords with comprehensive coverage are far better equipped to avoid crippling financial setbacks.

On top of that, many disaster-related repair expenses may qualify as tax deductions, offering some financial relief. Regularly reviewing your policy with an insurance agent ensures your coverage keeps up with rising property values and shifting local risks. These steps may feel like extra effort now, but they’ll pay off when you need them most.

7. Install Backup Systems and Redundancies

When disaster hits, having backup systems in place can mean the difference between a minor hiccup and a complete catastrophe. Electric generators are indispensable for keeping operations running during power outages, particularly in regions prone to hurricanes or severe storms. For even more independence, solar power systems can allow your property to operate entirely off-grid when municipal power grids fail. A prime example of this is Babcock Ranch in Florida, which maintained power during Hurricane Ian thanks to buried electrical lines and solar arrays, even as surrounding areas experienced widespread outages and damage. These backup power solutions lay a solid foundation for additional systems that protect your property’s structure and ensure business continuity for your rental properties.

Risk Mitigation Effectiveness

Florida's strict building codes have proven their worth during disasters. During Hurricane Ian, these codes reportedly saved between $1 billion and $3 billion in structural damage. Ian Giammanco, Ph.D., Managing Director of Standards & Data Analytics at IBHS, highlighted this impact:

"During Hurricane Ian, we estimated the Florida building code saved $1 billion to $3 billion in structural damage avoidance alone".

Beyond power solutions, underground utility lines offer another layer of protection, shielding wires from wind and debris to keep properties operational even after severe storms. In wildfire-prone areas, simple upgrades like installing metal mesh screens on attic and crawlspace vents can block embers - a key ignition source - providing a straightforward yet effective defense against fire damage. These measures not only protect your property but also help reduce recovery costs significantly.

Cost of Implementation

While installing backup systems requires an initial investment, financial assistance programs can help offset these costs. For example, NFIP policyholders may qualify for up to $30,000 through ICC coverage, and the SBA offers disaster loans with increased limits of up to 20%. On a state level, Alabama’s "Strengthen Alabama Homes" grant provides up to $10,000 for wind-mitigation upgrades, including reinforced roofs and impact-resistant windows. These programs make it easier to implement protective measures that can save you money in the long run by minimizing disaster-related losses.

Long-Term Benefits for Property Resilience

Properties equipped with redundant systems recover faster and are more appealing to tenants. Augie Williams-Eynon, Manager of the Urban Land Institute's Randall Lewis Center for Sustainability in Real Estate, emphasizes this point:

"Resilient buildings are more valuable buildings. Resilient homes make securing financing easier; they attract a high-quality tenant and when a disaster strikes, they reduce losses".

Additionally, installing sewer backflow valves can prevent sewage from entering your property during floods, protecting tenant health and preserving interior finishes. These proactive investments not only enhance your property’s ability to withstand disasters but also ensure smoother operations and greater tenant satisfaction in the aftermath.

8. Use Technology for Monitoring and Alerts

Modern technology makes it easier than ever to stay informed about potential disasters. Free mobile apps like the FEMA App send real-time weather alerts and disaster updates straight to your phone. No need for extra hardware - just download the app, and you’ll get immediate notifications about hazards in your area. These tools connect you to critical safety information from the National Weather Service and local emergency management agencies, helping you stay prepared and informed.

Risk Mitigation Effectiveness

Using monitoring technology can significantly reduce property damage and speed up recovery efforts. In fact, for every $1 spent on disaster mitigation, $6 is saved in future losses. Digital platforms for investing in rental properties also play a key role during emergencies by streamlining communication. Nick Thornton, Head of Operational Resilience for Global Banking at J.P. Morgan, highlights the importance of preparation:

"You can't practice in the middle of an incident".

To ensure systems work when needed, property owners should regularly test notification systems, such as emergency call trees and alert mechanisms, by running simulations.

Cost of Implementation and Ease of Adoption

Many monitoring tools, including mobile alert apps, are free or come at minimal cost. Digital maintenance management platforms offer added benefits, like tracking repair progress, storing expense records, and maintaining open communication with tenants. These features become especially valuable when filing insurance claims after a disaster.

Long-Term Benefits for Property Resilience

Properties equipped with monitoring technology tend to recover more quickly after disasters. Keeping digital records simplifies insurance claims, while automated maintenance tracking can identify system vulnerabilities before they become major issues. As Thornton puts it, "Resilience isn't a niche thing - resilience is everybody's business". Clear communication with tenants during emergencies is essential, and integrating these tools into your preparedness plan strengthens your overall disaster strategy. This also sets the stage for building stronger community partnerships in the next step.

9. Build Community Partnerships for Support

Securing federal disaster mitigation funds often hinges on working with local agencies. For example, programs like FEMA's Hazard Mitigation Assistance require applications to go through local government bodies. Partnering with local emergency management teams is essential for accessing this financial support and ensuring your resilience projects get off the ground. These collaborations also provide access to vital data, like Base Flood Elevation (BFE) details and local Flood Insurance Rate Maps, which are crucial for accurate risk assessments and planning. By fostering these relationships, you can unlock cost savings and operational resources that make a real difference.

Risk Mitigation Effectiveness

Teaming up with local officials can lead to tangible financial advantages. Across the U.S., more than 1,500 communities participate in FEMA's National Flood Insurance Program's Community Rating System (CRS). This program encourages communities to adopt flood management practices that go beyond the basics, rewarding property owners in these areas with discounted flood insurance premiums. FEMA emphasizes the broader impact of mitigation efforts:

"Mitigation... allows you to return home more quickly after a disaster. Mitigation also happens at the community level, where it can help your community thrive in the face of disasters and climate change."

Cost of Implementation and Ease of Adoption for Property Owners

Building partnerships with local agencies doesn’t require much beyond your time and initiative. Just as structural upgrades and emergency plans fortify your property, these collaborations extend those protections through a coordinated community approach, much like how you can invest in rental properties that are already managed for resilience. A good first step? Reach out to your local floodplain manager before making any structural changes. They can guide you on properly elevating electrical and mechanical systems to meet safety standards. If your property sustains significant damage, local officials can also help you navigate compliance requirements, potentially unlocking up to $30,000 in Increased Cost of Compliance (ICC) coverage. Additionally, the U.S. Small Business Administration offers disaster loans that can be increased by 20% to fund upgrades aimed at protecting against future disasters.

Long-Term Benefits for Property Resilience

Community partnerships are a cornerstone of long-term property resilience. Collaborating with groups like the Community Emergency Response Team (CERT) can provide specialized training for both property owners and tenants, equipping everyone with the skills to respond effectively to emergencies. Local building departments also play a critical role, ensuring that any structural changes align with current regulations, which helps you avoid expensive compliance issues down the road. These partnerships create a network of support, streamlining recovery efforts and reducing risks, while enhancing your broader risk management strategies.

10. Invest in Fractional Ownership to Spread Risk

In addition to physical improvements and operational safeguards, financial strategies can play a key role in strengthening your property's resilience.

How Fractional Ownership Reduces Risk

Fractional ownership helps manage disaster-related risks by spreading investments across multiple properties and locations. Instead of tying up all your capital in a single rental property - which might be vulnerable to region-specific threats like hurricanes or floods - you can diversify across different markets and climates. This geographic spread minimizes the financial impact of localized disasters. Plus, Real Estate Investment Trusts (REITs) often distribute a significant portion of their taxable income as dividends, offering steady cash flow to investors.

Lower Cost of Entry

Fractional ownership significantly lowers the financial barrier to real estate investment. For example, real estate syndication opportunities often start at around $50,000, giving you access to high-quality properties without requiring six- or seven-figure commitments. Platforms like Lofty make it even easier by allowing investors to purchase small fractions of rental properties across the U.S., eliminating the need for large down payments. Furthermore, these platforms or sponsors handle much of the day-to-day property management, letting you focus on building a diversified portfolio. This streamlined process creates a more accessible and passive way to invest.

A Passive Investment Opportunity

One of the biggest advantages of fractional ownership is its hands-off nature. Sponsors or investment firms take care of tasks like property acquisition, management, and operational improvements. This setup allows investors to transition from smaller residential properties to commercial real estate without needing extensive expertise in every market or asset type. The trade-off? You’ll have less control over individual property decisions compared to owning a property outright. To ensure a trustworthy investment, thoroughly vet the sponsor’s track record and review all legal documents - such as the Private Placement Memorandum - with a qualified legal professional. As Edinhart Realty emphasizes:

"A reputable sponsor will invest a significant amount of their own capital into the deal alongside their investors. This alignment of interests ensures they are motivated to make the project a success".

Long-Term Advantages for Resilience

From a disaster preparedness perspective, fractional ownership strengthens your financial stability. By pooling resources with other investors, you gain access to institutional-grade properties that might otherwise be unattainable. For instance, multi-family properties - often favored in fractional investments - typically maintain occupancy rates above 95%, providing a steady income stream even during regional challenges. Additionally, Alliance CGC reports a historical internal rate of return (IRR) of 28% across diversified asset classes for its investors. With professional management teams overseeing these assets, fractional ownership not only diversifies your portfolio but also supports investments in properties equipped with structural upgrades, emergency systems, and comprehensive disaster preparedness plans.

Conclusion

Building resilient rental properties is a smart way to safeguard your finances and ensure tenant safety. The strategies discussed - like conducting risk assessments, installing backup systems, and crafting emergency plans - work together to minimize potential losses and maintain operations. Here's a compelling fact: for every $1 spent on disaster mitigation, you save $6 in future costs. That’s not just good financial planning - it’s a necessity in today’s world, where natural disasters are becoming more frequent and expensive.

In 2022 alone, disasters caused $32 billion in global economic losses, but only $14 billion of that was insured. This highlights the importance of comprehensive risk management. Without proper insurance and financial reserves, landlords face significant financial risks and liabilities after disasters. As FEMA’s Myra Shird wisely states:

"It is safer, cheaper, and ultimately much easier to limit future destruction than to repair it afterward".

Start by identifying the specific risks in your region - whether it’s hurricanes, floods, wildfires, or severe winter storms. Use vacancy periods to make structural upgrades without disrupting tenants, and review your insurance annually to ensure it covers the most relevant risks for your area. Clear communication and preparedness training can also make a huge difference when emergencies strike.

Beyond physical preparations, diversifying your investments adds another layer of protection. Spreading your investments across different regions reduces your exposure to localized disasters. For instance, platforms like Lofty let you invest in rental properties across various U.S. markets, helping to maintain steady income streams while lowering regional risk. Combining property upgrades, solid emergency plans, and diversified investments creates a strong shield against nature’s unpredictability.

FAQs

How can I identify the natural disaster risks for my rental property?

When evaluating the risks of natural disasters for your rental property, the first step is to research the specific hazards tied to its location. Is the property in a flood zone? Does the area have a history of wildfires, hurricanes, or tornadoes? Local government websites and emergency management agencies often provide hazard maps and detailed historical data to help you answer these questions.

It’s also a good idea to dig into the area’s past disaster events and carry out regular property inspections. Look for issues like poor drainage systems or structural problems that could make the property more vulnerable. By blending local hazard data with consistent property evaluations, you can take smarter steps to safeguard your investment against potential threats.

What are the most affordable ways to make a rental property more disaster-resistant?

Improving the resilience of a rental property doesn’t have to drain your wallet. There are several affordable upgrades that can make a big difference in protecting against natural disasters. For properties in flood-prone areas, simple steps like raising electrical outlets, appliances, and HVAC systems at least a foot above the base flood level can help prevent water damage. Anchoring fuel tanks and elevating key electrical components are also low-cost solutions that could save you from expensive repairs down the road.

When it comes to storm protection, reinforcing garage doors and installing storm shutters or shatter-resistant window films can provide a strong defense against high winds and debris. These upgrades are budget-friendly and can significantly reduce the risk of damage. For homes in areas prone to flooding, elevating the entire property is a bigger investment, but it can lead to lower insurance premiums and long-term safety. By prioritizing these practical improvements, property owners can boost their property's resilience without overspending.

How does fractional ownership reduce risk in rental property investments?

Fractional ownership offers a practical way to reduce risk in real estate investing. By spreading your investment across multiple rental properties, you’re not putting all your eggs in one basket. If one property faces unexpected damage or loss, the financial impact is cushioned by the performance of the others.

This strategy not only helps manage risk but also allows you to enjoy the benefits of property value growth and rental income. Plus, it eliminates the need for large upfront investments or the hassle of hands-on property management, making real estate more accessible and less stressful.

Related Blog Posts