Interest Rates vs. REIT Performance

Jerry Chu

REITs (Real Estate Investment Trusts) give you a way to invest in fractional real estate without owning property directly. But how do interest rates impact their performance? Here’s the short answer:

- Low interest rates: REITs borrow cheaply, boosting margins and making their dividends more attractive than bonds. Sectors like healthcare and data centers benefit most.

- High interest rates: Borrowing costs rise, but REITs often thrive if the economy is growing. Rent increases and occupancy gains can offset rate hikes.

- Rate cuts: Historically, REITs deliver strong returns (9.48% annualized) in the 12 months after a rate cut, outpacing stocks.

- Rate hikes: While higher rates pressure valuations, REITs have posted positive returns in 78% of rising rate periods since 1992.

2026 outlook: With the Federal Reserve easing rates, REITs are well-positioned. Growth sectors like healthcare and residential REITs are thriving, while fixed-rate debt shields many REITs from immediate rate changes.

Key takeaway: Focus on REITs with strong rent growth, low leverage, and sectors aligned with the economic cycle. Diversification across REIT types and regions can help manage risks.

REIT Performance in Different Interest Rate Environments: Historical Returns and Key Statistics

2 Ways Higher Interest Rates Affect REITs

sbb-itb-a24235f

How Interest Rates Impact REIT Valuations and Borrowing Costs

Grasping how interest rates influence both property values and borrowing expenses is key to understanding their effect on REIT performance.

Interest Rates and REIT Valuations

Interest rates impact REIT valuations mainly through capitalization rates (cap rates) and discount rates. When interest rates rise, cap rates tend to increase, which lowers property values. The formula is straightforward: property value equals net operating income (NOI) divided by the cap rate. If the NOI stays the same, a higher cap rate means a lower valuation.

"If a property generates $100,000 in net operating income and the prevailing cap rate rises from 5% to 6% due to an interest rate hike, the property's value drops from $2 million to about $1.67 million."

– Trey Webb, Partner, Bennett Thrasher

On top of that, higher discount rates reduce the present value of future cash flows. Rising interest rates also increase financing costs, which makes new property developments more expensive. This can limit supply, indirectly helping to sustain the value of existing assets. These interconnected factors highlight how valuations and borrowing costs are intertwined.

Borrowing Costs and REIT Growth

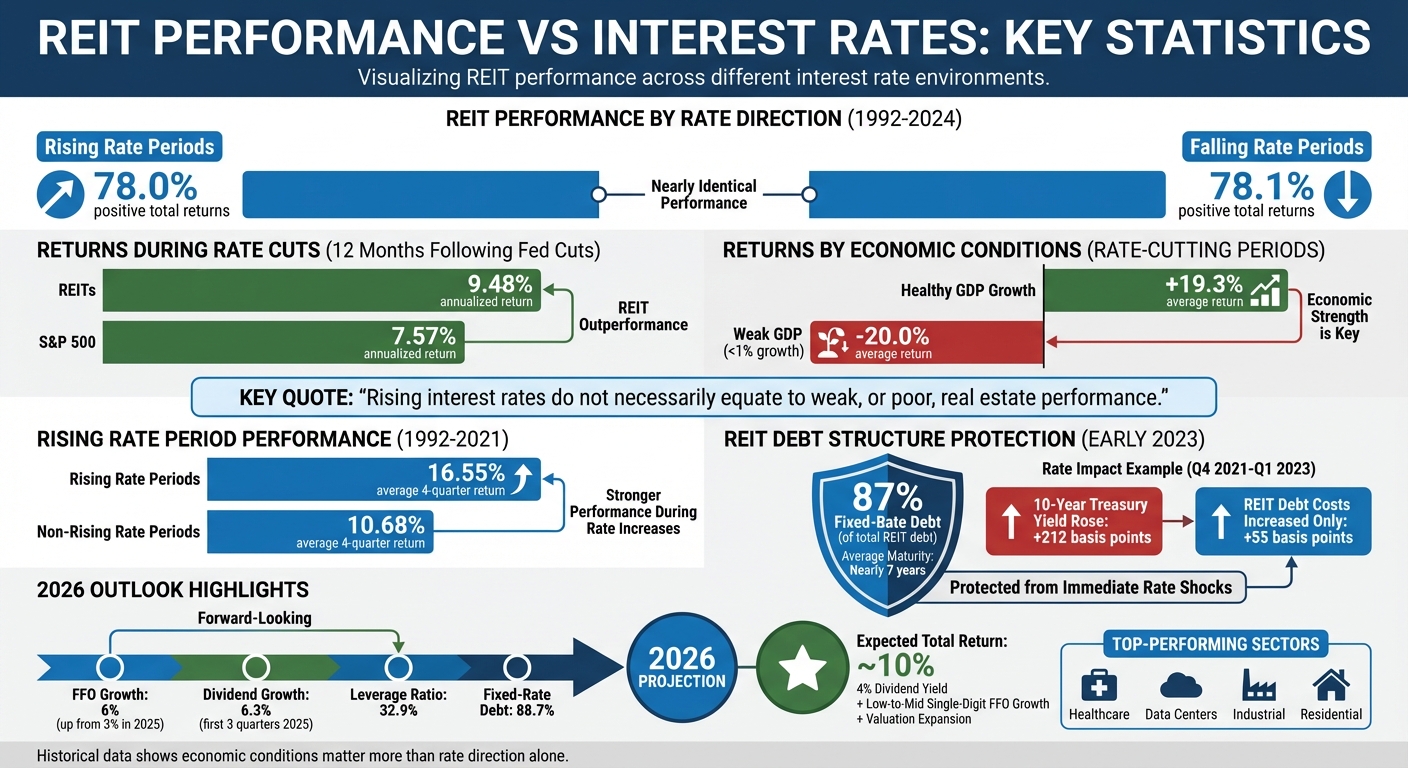

Interest rate changes directly affect how much it costs REITs to borrow. As of early 2023, 87% of REIT debt was fixed-rate, with an average maturity of nearly seven years. This setup shields many REITs from the immediate impact of rising rates.

For example, between Q4 2021 and Q1 2023, the 10-year Treasury yield jumped by 212 basis points. Yet, the average interest rate on REIT debt increased by only 55 basis points during the same period. This relative stability is thanks to careful debt management. REITs often stagger debt maturities, avoiding situations where they need to refinance large portions of their portfolio during high-rate periods. Conversely, when rates drop, refinancing high-interest debt can improve cash flow and free up funds for new investments.

"With access to the public markets, REITs have a built-in advantage in times of constrained credit through the ability to raise capital via seasoned equity or unsecured bond issues."

– Greg MacKinnon, Research Director, Pension Real Estate Association (PREA)

These strategies not only help manage borrowing costs but also bolster confidence among investors, tying back to how valuations and demand are influenced.

Investor Demand for REITs in Different Rate Environments

Investor interest in REITs often depends on how their dividend yields stack up against other income-producing assets, like Treasury bonds. When rates rise, higher bond yields can make REITs seem less appealing. This "bond-proxy" perspective causes shifts in investor demand based on changes in the fixed-income market.

Since 2022, REIT performance has generally moved inversely to 10-year Treasury yields. However, the economic backdrop matters. In times of strong economic growth, increased rental income and higher occupancy rates can offset rising borrowing costs. Additionally, expensive financing can limit new construction, helping to maintain the value of existing properties. As these factors interplay, investor sentiment adjusts, reflecting the broader rate environment and economic conditions.

REIT Performance During Rate Cuts vs. Rate Increases

This section dives into how REITs perform during periods of rate cuts versus rate increases, building on earlier insights into valuation and financing. While interest rates play a role, the broader economic backdrop often has a greater influence on REIT success. Between Q1 1992 and Q4 2024, REITs delivered positive total returns in 78.0% of rising rate periods and 78.1% of falling rate periods. These figures highlight that interest rate direction alone isn't the main driver of REIT performance - economic conditions carry more weight.

Historical Data: REITs During Rate-Cutting Cycles

Rate cuts don't automatically translate to strong REIT performance. The surrounding economic environment is what truly matters. For example, during rate-cutting periods from 1992 to 2024, REITs achieved an average 19.3% four-quarter return when GDP growth was healthy. However, when GDP growth dipped below 1%, returns plummeted to an average of -20.0%.

"Falling yields and weak economies have often been a recipe for poor REIT returns."

– Edward F. Pierzak, Senior Vice President of Research, Nareit

Lower interest rates can reduce borrowing costs and boost property values, but these benefits are often overshadowed when rate cuts signal economic trouble. In such cases, tenant demand declines, occupancy rates drop, and property fundamentals weaken.

REIT Challenges During Rising Rate Periods

Rising rates bring their own set of challenges, yet REITs have shown resilience in many rate-hiking cycles. Investors sometimes view REITs as "bond proxies", leading to capital shifts toward higher-yielding Treasuries. Rising rates can also increase discount rates, pressuring valuations, and make refinancing debt more expensive. Despite these hurdles, REITs have historically delivered strong returns in such periods. Between 1992 and 2021, REITs averaged a 16.55% four-quarter return during rising rate periods, compared to 10.68% in non-rising rate periods. They even outperformed the S&P 500 in 50% of rising rate episodes during this timeframe.

When rate hikes are aimed at cooling an overheated economy, the accompanying economic strength often supports higher occupancy rates and rent growth. Additionally, many modern REITs have adopted fixed-rate debt structures, which protect them from immediate rate increases.

Case Study: REIT Behavior in Past Economic Cycles

History shows how REITs have performed across different economic cycles. For instance, between December 1976 and September 1981, the 10-year Treasury yield jumped by 840 basis points, yet REITs delivered a cumulative total return of 121.7%, surpassing the S&P 500's 91.4% return. Similarly, from October 1993 to November 1994, Treasury yields climbed by 270 basis points, and REITs returned 50.9%, while the S&P 500 saw a 10.4% loss.

The story is different when rates fall during economic weakness. In these cases, such as the "Quadrant III" scenario (falling rates and weak GDP growth), REITs averaged -20.0% returns. This highlights how declining rates can't offset the challenges of reduced tenant demand and struggling property fundamentals.

"Rising interest rates do not necessarily equate to weak, or poor, real estate performance."

– Edward F. Pierzak, Senior Vice President of Research, Nareit

Publicly traded REITs also tend to outperform private real estate investments, regardless of rate conditions. During high-rate periods (10-year Treasury yields of 4.80% to 7.09%), REITs averaged 14.91% annual returns, compared to private real estate's 9.41%, creating a performance gap of 5.50%. This advantage becomes even more pronounced as rates rise, thanks to REITs' liquidity and operational efficiencies.

Which REIT Sectors Are Most Sensitive to Rate Changes?

Not all REIT sectors react the same way to shifts in interest rates. Some thrive when borrowing costs drop, while others face challenges when rates rise. Knowing these differences can help investors make smarter decisions as the Federal Reserve adjusts its monetary policy.

REIT Sectors That Benefit From Low Interest Rates

Sectors like data centers, telecom infrastructure, and health care REITs perform well when interest rates are low. These sectors share two important traits: they require large amounts of capital to expand and typically rely on long-term leases with tenants.

Lower rates allow these capital-heavy sectors to refinance debt at better terms and fund new projects more affordably. For example, data centers often need upgrades to meet the growing demand for cloud computing, and reduced borrowing costs make these expansions more economical. Similarly, health care REITs, which lease properties to hospital systems and senior care operators, benefit from stable, long-term cash flows. At the same time, lower discount rates can boost the value of their properties.

"Data centers, telecom infrastructure, and health care REITs have historically benefited the most from lower rates due to long-duration leases and capital-intensive models." – Invesco

The data backs this up. After a Federal Reserve rate cut, U.S. REITs delivered an average annualized return of 9.48% over the following 12 months, surpassing the S&P 500's 7.57%. As of early 2023, 87.0% of REIT debt was fixed-rate, meaning these sectors could take advantage of falling market rates for new borrowing without impacting their existing debt costs.

REIT Sectors That Struggle With Rising Rates

Some REIT sectors, particularly those with bond-like characteristics - low growth potential and fixed long-term leases - face more challenges when interest rates climb. These sectors often lack the earnings growth needed to offset higher discount rates.

Lodging and hotel REITs, however, are less affected by rate changes. Their performance depends more on travel demand and the broader economy than on financing costs. Unlike sectors with multi-year leases, hotels adjust pricing daily based on occupancy, making them less sensitive to rate shifts.

Apartment REITs occupy a middle ground. Residential properties benefit from consistent demand, but their shorter lease terms (usually one year) limit the boost they get from falling rates. On the flip side, these shorter leases allow for quicker rent adjustments during inflationary periods. Sectors with shorter leases or strong demand growth, like data centers and industrial properties, can adjust rents faster to keep up with inflation. In contrast, traditional net-lease sectors often face more pressure on valuations.

Diversification Strategies for REIT Investors

Given the varied ways REIT sectors respond to interest rate changes, diversification is key to managing risk. Instead of focusing on one property type, investors can balance rate-sensitive sectors with those driven by broader economic trends.

A balanced portfolio might include growth sectors like data centers and industrial properties, paired with stable income sectors such as health care and retail. Growth sectors can boost cash flow to counter rising discount rates, while income-focused sectors offer stability through long-term leases. Another smart move is to prioritize REITs with staggered, fixed-rate debt to avoid sudden spikes in interest costs as rates climb.

Geographic diversification also plays a role. REITs operating across different regions can provide a hedge against localized economic downturns or shifts in property demand. Since REITs are required to distribute at least 90% of their taxable income to shareholders, metrics like the debt-to-market asset ratio (averaging around 32.8% for the industry) can help investors gauge a REIT's sensitivity to rate changes.

Tailoring your portfolio to the economic cycle is another effective strategy. When rates rise alongside strong GDP growth, REITs with shorter leases or inflation-indexed rents can adjust revenues quickly. On the other hand, during periods of falling rates and weaker economic conditions, stable sectors with long-term contracts often deliver more reliable returns.

2026 Outlook: Interest Rates and REIT Performance This Year

Current Economic Conditions and Federal Reserve Policy

As 2026 begins, the Federal Reserve’s target interest rate range sits at 3.50%–3.75%, following a series of rate cuts throughout 2024 and 2025. The Fed appears to be favoring a cautious approach, with expectations of holding steady early in the year before potentially lowering rates further to 3.00%–3.25%.

Adding some uncertainty to the outlook is the upcoming expiration of Fed Chair Jerome Powell's term on May 15, 2026. A more dovish successor could increase the likelihood of additional rate cuts. Meanwhile, the 10-year Treasury yield has remained stable between 4.00% and 4.25% since August 2025, serving as a key reference point for real estate underwriting. Inflation seems to be settling around 3%, largely due to moderated rent growth and stable housing costs, which account for 44% of the Consumer Price Index.

"The experience of 2025 reinforced an important lesson... Capital deployment responded not simply to lower rates, but to greater confidence in the forward path of policy." - Scott Williams, Aline Capital

These economic dynamics are shaping valuation models and investor strategies, underscoring the importance of keeping a close eye on REIT performance metrics. This sets the stage for a promising year for REIT fundamentals in 2026.

REIT Fundamentals in 2026: Growth and Stability

REITs are entering 2026 with strong momentum. Funds from operations (FFO) growth is projected to reach nearly 6%, a significant jump from the 3% growth seen in 2025. Additionally, REIT dividends grew by 6.3% during the first three quarters of 2025 compared to the same period in 2024.

The sector remains financially sound, with a leverage ratio of 32.9% and 88.7% of total debt locked in at fixed rates, shielding it from immediate rate fluctuations. The public-private real estate cap rate spread stood at 112 basis points in Q3 2025, hinting at a potential valuation alignment this year. Historically, narrowing spreads have led public REITs to outperform private real estate by an average of 41.7% over the following four quarters.

Adding to the optimism, Fannie Mae and Freddie Mac have increased their 2026 lending caps by over 20%, reaching $88 billion each, which bolsters market liquidity. This creates an opening for REITs to pursue acquisitions as transaction activity picks up.

"We think investment activity should improve as more real estate assets start to trade again and offer REITs the opportunity to drive growth - hence the acceleration into 2026." - Anthony Paolone, Co-head of U.S. Real Estate Stock Research, J.P. Morgan

With these strong fundamentals in place, targeted investment opportunities are emerging across various REIT sectors.

Investment Opportunities in the 2026 REIT Market

Certain REIT sectors are particularly well-positioned for growth this year. Healthcare REITs, especially those focused on senior housing, are benefiting from aging demographics, with the first wave of baby boomers turning 80 in 2026. These REITs are seeing double-digit organic growth. Meanwhile, medical office buildings continue to perform well, boasting vacancy rates of just 7.4%, compared to 13.9% for traditional office spaces.

Net lease REITs, which are highly sensitive to interest rate changes, remain appealing with dividend yields typically exceeding 5% - a strong draw as rates decline. Residential REITs are also set for a recovery as the pace of new construction slows and previously delivered units are absorbed. In the retail space, grocery-anchored properties are proving resilient, maintaining occupancy rates 4% higher than their non-anchored counterparts.

Even the struggling office sector may be nearing a turning point, with vacancy rates expected to peak in early 2026. For investors looking beyond U.S. markets, global diversification offers compelling returns. In 2025, Asia delivered 28.0%, and Europe achieved 19.9%, both far outpacing the U.S. market’s 4.5%.

"We believe a combination of 4% dividend yields, low-to-mid-single-digit FFO growth and some room for valuation to expand could result in approximately a 10% total return." - Anthony Paolone, Co-head of U.S. Real Estate Stock Research, J.P. Morgan

For those exploring fractional real estate investments, platforms like Lofty (https://lofty.ai) offer a modern approach. These platforms allow individuals to invest in rental properties across the U.S. without the need for large down payments, offering diversification and liquidity through instant buy-and-sell options.

Conclusion: Investing in REITs as Interest Rates Change

Key Points to Remember

When it comes to REIT performance, the focus should be on operating fundamentals rather than the direction of interest rates. Historical trends show that REITs achieved positive total returns in 78% of months with rising Treasury yields between 1992 and 2025. This performance is driven by factors like net operating income, rent growth, and occupancy levels - not just interest rate fluctuations.

The state of the economy plays a bigger role than rate changes alone. When interest rates rise alongside a strengthening economy, REITs often thrive due to increased space demand and higher rental income. The REIT industry is also well-positioned to handle rate increases, with a median of 83% of debt at fixed rates and average maturities exceeding 87 months. Different sectors respond differently to rate changes: for example, data centers and healthcare REITs perform well during rate cuts, while industrial and residential REITs excel during economic growth.

"Rising interest rates do not necessarily equate to weak, or poor, real estate performance." – Edward F. Pierzak, Vice President of Investment Research, Nareit

Armed with these insights, investors can take a more informed approach to navigating the market.

How Investors Can Adjust Their Strategies

To make the most of changing market conditions, investors should focus on fundamentals rather than attempting to predict interest rate movements. Look for REITs with strong operational metrics, such as rising occupancy rates, steady rent growth, and low leverage ratios. Historical data shows that during periods of rate easing, REITs have delivered average returns of 9.48% in the 12 months following Federal Reserve easing cycles. In such environments, sectors like net lease and healthcare, which benefit from lower financing costs, are worth considering.

Adjusting investments based on the economic cycle can also be effective. During economic expansions, industrial and residential REITs often see growth due to higher demand. In contrast, during economic slowdowns, defensive sectors like healthcare and residential REITs, which cater to essential services, tend to provide stability. Evaluating debt structures is equally important - REITs with high fixed-rate debt and staggered maturities are better equipped to handle refinancing risks as market conditions shift.

For those looking to diversify beyond traditional REITs, platforms like Lofty offer fractional ownership in U.S. rental properties. This option provides liquidity and the potential for property appreciation without the large upfront costs of direct real estate investments. Whether through public REITs or fractional ownership, navigating 2026’s transitional rate environment will require a balance between yield opportunities and long-term growth potential.

FAQs

Why do REITs sometimes rise when interest rates rise?

When interest rates go up, REITs can still perform well. Why? Higher rates often point to a growing economy. A stronger economy can lead to higher occupancy rates, rising rents, and property value growth. These benefits can sometimes offset the downside of higher borrowing costs for REITs.

Which REIT sectors are most rate-sensitive?

The REIT sectors most affected by interest rate changes are typically those with higher leverage and shorter lease durations. This includes sectors like lodging, retail, and office spaces. These areas feel the impact more because they often rely heavily on debt financing and operate with lease structures that renew over shorter timeframes, making them more sensitive to rate fluctuations.

How can I reduce interest-rate risk in a REIT portfolio?

To manage interest-rate risk in a REIT portfolio, prioritize REITs with solid balance sheets and lower levels of debt. These REITs are typically more resilient during periods of rising interest rates. Diversification is another important strategy - spread your investments across different REIT sectors or consider REIT ETFs for broader market coverage. You can also adjust your portfolio based on the current rate environment by focusing on sectors that are less affected by rate changes or using hedging strategies. Staying proactive and maintaining a diversified approach are essential for keeping risk in check.

Related Blog Posts