'/%3e%3cpath%20d='M110.5%2074.84L61.56%20113.3V150.04H0V87.4L110.5%200V74.84Z'%20fill='url(%23paint1_linear_1102_1766)'/%3e%3cpath%20d='M159.44%20150.04L159.44%20205.81H159.2L110.5%20166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57L159.44%20150.04Z'%20fill='url(%23paint2_linear_1102_1766)'/%3e%3cpath%20d='M110.5%20110.57V166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57Z'%20fill='url(%23paint3_linear_1102_1766)'/%3e%3cpath%20d='M159.44%20206H61.5601L61.8001%20205.81L110.5%20166.53L159.2%20205.81L159.44%20206Z'%20fill='url(%23paint4_linear_1102_1766)'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1102_1766'%20x1='166'%20y1='-19.908'%20x2='145.641'%20y2='227.731'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.723958'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_1102_1766'%20x1='64'%20y1='15.7891'%20x2='172.309'%20y2='257.652'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%239383FF'/%3e%3cstop%20offset='0.75'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_1102_1766'%20x1='171.462'%20y1='36.6188'%20x2='8.598'%20y2='270.272'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.229167'%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.994792'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_1102_1766'%20x1='55.7219'%20y1='-31.3876'%20x2='76.8187'%20y2='349.172'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.307292'%20stop-color='%239383FF'/%3e%3cstop%20offset='0.854167'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_1102_1766'%20x1='110'%20y1='271'%20x2='76.5255'%20y2='202.314'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.90625'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cpath%20d='M110.5%2074.84L61.56%20113.3V150.04H0V87.4L110.5%200V74.84Z'%20fill='url(%23paint1_linear_1102_1752)'/%3e%3cpath%20d='M159.44%20150.04L159.44%20205.81H159.2L110.5%20166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57L159.44%20150.04Z'%20fill='url(%23paint2_linear_1102_1752)'/%3e%3cpath%20d='M110.5%20110.57V166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57Z'%20fill='url(%23paint3_linear_1102_1752)'/%3e%3cpath%20d='M159.44%20206H61.5601L61.8001%20205.81L110.5%20166.53L159.2%20205.81L159.44%20206Z'%20fill='url(%23paint4_linear_1102_1752)'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1102_1752'%20x1='166'%20y1='-19.908'%20x2='145.641'%20y2='227.731'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.723958'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_1102_1752'%20x1='64'%20y1='15.7891'%20x2='172.309'%20y2='257.652'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%239383FF'/%3e%3cstop%20offset='0.75'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_1102_1752'%20x1='171.462'%20y1='36.6188'%20x2='8.598'%20y2='270.272'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.229167'%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.994792'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_1102_1752'%20x1='55.7219'%20y1='-31.3876'%20x2='76.8187'%20y2='349.172'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.307292'%20stop-color='%239383FF'/%3e%3cstop%20offset='0.854167'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_1102_1752'%20x1='110'%20y1='271'%20x2='76.5255'%20y2='202.314'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.90625'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

Why do syndications need custom debt terms? Syndications involve multiple lenders financing large-scale projects, making standard loan agreements too rigid for shared ownership and varied risk preferences. Custom debt terms help streamline decision-making, manage risks, and ensure smoother operations.

Key Takeaways

- Syndications differ from single-lender deals: They spread risk across multiple lenders, making them ideal for large transactions but requiring tailored agreements.

- Challenges without customization: Delays in decisions, intercreditor conflicts, and funding shortfalls can derail projects.

- How customization works: Focus areas include consent thresholds, intercreditor agreements, and payment priorities to align lender interests.

Quick Overview

- Loan Structure: Syndicated loans use roles like lead arrangers, agents, and syndicate members to distribute risk and responsibilities.

- Debt Types: Options include A/B loans, mezzanine debt, and senior-subordinate notes, each suited to different risk levels and project needs.

- Market Context: With $1.1 trillion in maturing mortgage debt (2024), custom terms are increasingly critical for large-scale financing.

Customizing debt terms ensures smoother syndication deals by addressing complex lender dynamics and project requirements.

How to Structure a Debt Fund: Real Estate Syndication & PPM Best Practices

How Syndication Loans Are Structured

Syndicated loans bring together multiple lenders under a single agreement, creating a more intricate setup compared to traditional one-on-one lending. This structure relies on defined roles and tiers, making it essential to understand how these loans are organized.

Main Elements of Syndicated Loans

Syndicated loans are built on a three-tier framework:

- Borrower Facility: The overarching master agreement.

- Tranches: Specific portions of the loan, each with unique terms.

- Drawdowns: The actual disbursement of funds.

Key participants play distinct roles in this structure:

- The Lead Arranger (or Bookrunner): Responsible for structuring the deal, setting pricing, and marketing the loan. For their efforts, they typically earn 1% to 3% of the total loan commitment.

- Administrative Agent: Once the loan is finalized, this party oversees payment flows, distributes interest among syndicate members, and ensures compliance with covenants throughout the loan’s 5–7 year term.

- Syndicate Members: These include commercial banks, hedge funds, and collateralized loan obligations (CLOs). They provide the loan capital and share the credit risk proportionally.

- Trustee: Holds the collateral on behalf of the syndicate, simplifying enforcement if issues arise.

These roles shape the various facility types designed to meet investor preferences. For example:

- Term Loan A (TLA): Popular with commercial banks, this loan involves substantial quarterly repayments over about five years.

- Term Loan B (TLB): Geared toward institutional investors, it features minimal annual repayments (around 1%) and a large lump-sum payment at maturity after 6–7 years.

- Revolving Credit Facilities (RCF): Short-term credit lines designed to address working capital needs.

A notable example of syndication in action is Tencent Holdings’ $4.65 billion loan in March 2017, coordinated by Citigroup. This deal involved commitments from a dozen banks, with Citigroup serving as the lead arranger and bookrunner. A year earlier, Tencent raised $4.4 billion through institutions like Citigroup, HSBC Holdings, and Bank of China.

Syndication vs. Conventional Lending

The differences between syndicated and conventional loans go beyond the number of lenders involved. In a conventional loan, one bank assumes all the risk. Syndicated loans, on the other hand, spread the risk across multiple institutions, making them ideal for large-scale transactions requiring $100 million or more. By 2022, the global syndicated loan market had surpassed $4 trillion in outstanding commitments.

Decision-making in syndicated loans reflects the proportional contributions of each lender. For instance, a lender providing 30% of the capital holds 30% of the voting power on amendments or waivers. To avoid deadlocks, borrowers often include “yank the bank” provisions, enabling them to replace dissenting lenders when a majority agrees on a change.

Another unique feature is market-flex language, introduced after the 1998 Russian financial crisis. This allows arrangers to adjust pricing or reallocate funds between tranches based on investor demand during the book-building process. Unlike conventional loans, this flexibility helps adapt to market dynamics effectively.

How to Customize Debt Terms in Syndications

Customizing debt terms in syndicated loans involves focusing on three main areas: consent thresholds, intercreditor agreements, and payment priorities. These elements play a crucial role in shaping how lenders work together, both in regular operations and during financial distress.

Setting Consent and Decision-Making Terms

In syndicated loans, certain key actions — like changing interest rates, adjusting principal amounts, extending maturity dates, or releasing collateral — require unanimous lender approval. To address this, modern agreements often include amend-and-extend provisions. These allow borrowers to extend loan maturities for consenting lenders, provided a minimum approval threshold is met. As Winston & Strawn LLP explains:

“Since it is often the case that such pro rata treatment provisions require supermajority or even unanimous lender approval for any waiver or amendment, lenders that were unwilling to consent could potentially hold up such transactions.”

This approach minimizes the power of dissenting lenders to block deals.

Minority lenders should ensure they secure sacred rights provisions, especially regarding lien subordination, not just lien release. While releasing collateral typically requires unanimous consent, subordinating liens may only need majority or supermajority approval, depending on the agreement’s terms. Borrowers also negotiate exceptions to standard pro rata sharing rules, like “open market purchase” or “Dutch auction” provisions. These allow non-pro rata debt buybacks without needing full lender approval.

Such consent provisions lay the groundwork for strong intercreditor agreements, which are essential for protecting lender interests.

Modifying Intercreditor Agreements

Intercreditor agreements (ICAs) are vital for managing lender relationships. They define cash flow priorities, collateral rights, and coordination during workouts or bankruptcy proceedings. As Finhelp.io highlights:

“Poorly drafted or absent ICAs, by contrast, commonly produce costly, time‑consuming disputes that erode recoveries and delay restructurings.”

Key features of ICAs include standstill periods, which usually last 90 to 180 days. These periods prevent junior lenders from interfering with senior lenders’ enforcement actions, like seizing collateral or filing bankruptcy petitions. Junior lenders also negotiate protections, such as limiting payment blockages to two per year and capping them at three or four over the loan’s lifetime. Additionally, caps on senior debt ensure that increases in loan amounts or fees require junior lender consent.

Buy-out rights provide further balance. These allow junior lenders to purchase the senior lender’s position at par value under specific circumstances, such as loan acceleration or insolvency. DLA Piper notes:

“The purchase option enables a junior lender to mitigate the deeper subordination terms to which it is subject if the senior lender is being overly accommodating to the borrower at the expense of the junior lender’s interests.”

Addressing intercreditor terms early, during the term sheet phase, helps avoid last-minute disputes that could delay closings. Turnover clauses are another key component, ensuring any creditor who receives payments in violation of the priority waterfall returns those funds to the senior creditor.

Structuring Default and Payment Waterfall Terms

Once consent and intercreditor frameworks are established, the next step is defining robust default and payment terms to ensure lender alignment during financial stress. Payment waterfalls specify how cash flows are distributed among lenders, both before and after default. Using templates from the Loan Syndications and Trading Association (LSTA) ensures compliance and clarity in these situations.

Covenant structures play a critical role in early intervention. “Covenant Heavy” agreements include multiple financial tests that alert lenders to potential issues before default, while “Cov-lite” structures are more borrower-friendly, with fewer tests. Pricing ratchets, which adjust interest rate spreads based on performance metrics like leverage ratios, help align borrowing costs with the borrower’s risk profile.

For off-balance sheet arrangements, risk participation agreements allow lenders to share loan exposure and returns while letting the lead lender act as the main point of contact. Accordion features also give borrowers the option to expand facility sizes under pre-agreed terms without disrupting existing payment priorities.

Agency fees, which compensate the lead bank for managing communications and collections during defaults, are typically predefined. These fees usually range from $10,000 to $50,000. Additionally, call protection provisions, whether soft or hard, ensure lenders maintain expected returns if borrowers refinance early during periods of declining interest rates.

| Fee Type | Typical Range |

|---|---|

| Commitment Fee | 10–50 bps |

| Upfront Fee | 25–100 bps |

| Agency Fee | $10,000–$50,000 |

| Leveraged Spreads | 300–500+ bps |

| Investment-Grade Spreads | 75–150 bps |

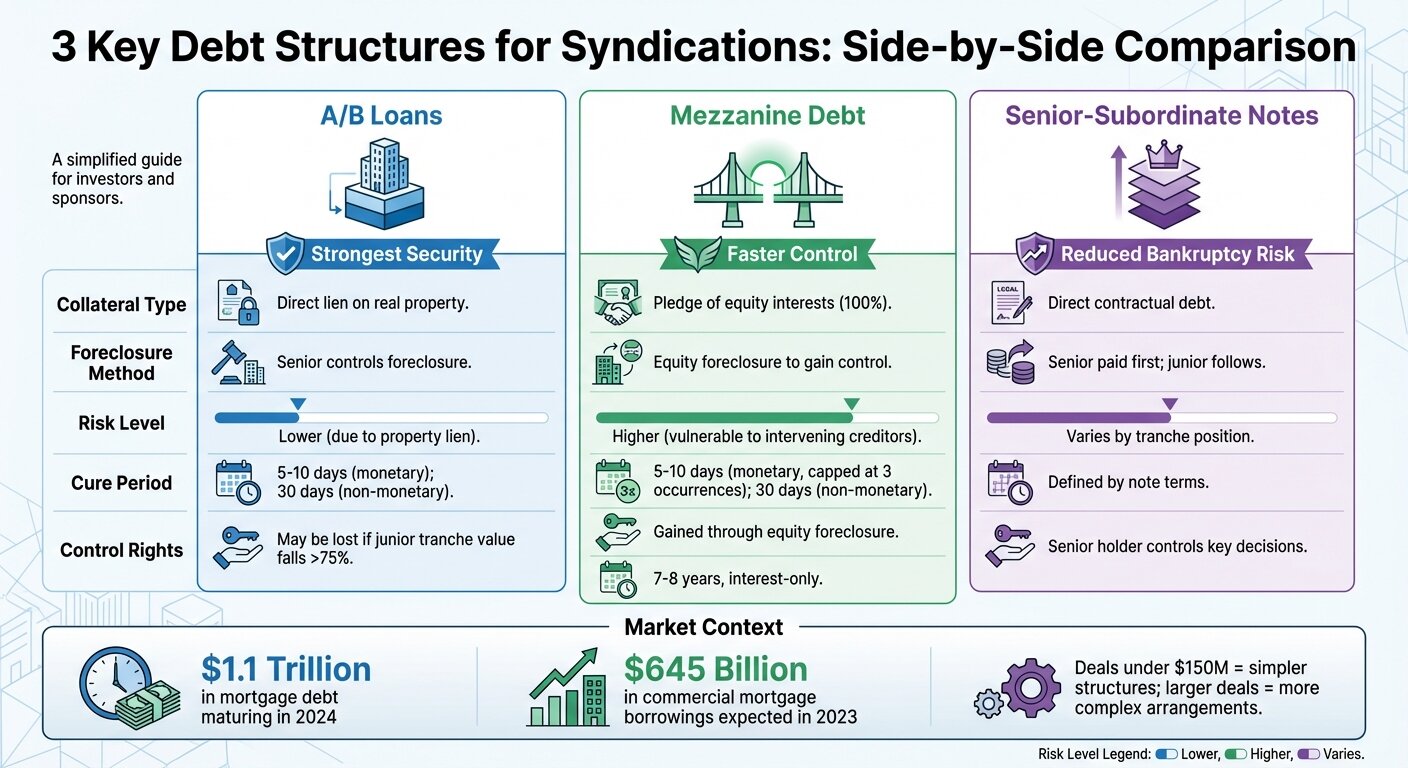

Comparing Debt Structures for Syndications

A/B Loans vs. Mezzanine Debt vs. Senior-Subordinate Notes

Choosing the right debt structure is a critical step in tailoring loan terms for syndications. Here’s a breakdown of three commonly used models and their unique features.

A/B loans split a mortgage into two parts: a senior (A) tranche and a junior (B) tranche, both secured by a direct lien on the property itself. This setup provides stronger security compared to mezzanine debt, as the collateral is tied directly to the real estate. However, if the junior tranche’s value drops by more than 75%, it triggers a Control Appraisal Event.

Mezzanine debt bridges the gap between senior loans and equity by using a 100% pledge of the equity interests in the entity owning the property. This structure allows lenders to act quickly by initiating equity foreclosure to take control. While this speed is an advantage, mezzanine lenders face greater exposure to intervening creditors. These loans typically run for seven to eight years, are interest-only with no amortization, and carry higher costs than senior debt but are generally cheaper than equity financing.

Senior-subordinate notes create a direct contractual relationship with the borrower and are treated as “debt” for regulatory purposes, reducing bankruptcy risks. In the event of a default, senior noteholders are paid in full before junior noteholders receive any funds. Both junior lenders in A/B loans and mezzanine lenders usually have cure rights, which are commonly set at 5 to 10 days for monetary defaults and 30 days for non-monetary defaults.

The scale of a deal often dictates the structure. Smaller club deals, typically under $150 million, are simpler, while larger transactions require more intricate arrangements. With an estimated $1.1 trillion in outstanding mortgage debt maturing in 2024, the need for adaptable structures like mezzanine financing is expected to rise.

| Feature | A/B Loans | Mezzanine Debt | Senior-Subordinate Notes |

|---|---|---|---|

| Collateral Type | Direct lien on real property | Pledge of equity interests | Direct contractual debt |

| Foreclosure Method | Senior controls foreclosure | Equity foreclosure to gain control | Senior paid first; junior follows |

| Risk Level | Lower due to property lien | Higher; vulnerable to creditors | Varies by tranche position |

| Cure Period | 5–10 days (monetary); 30 days (non-monetary) | Similar to A/B loans; monetary cures often capped at three occurrences | Defined by note terms |

| Control Rights | May be lost if junior tranche value falls >75% | Gained through equity foreclosure | Senior holder controls key decisions |

Conclusion: Main Points on Customizing Debt Terms

Customizing debt terms in syndications is all about aligning financing with your property’s cash flow and long-term goals. The best time to negotiate key aspects — like recourse carve-outs, leasing rights, and transfer provisions — is during the term sheet stage, when you have the most leverage.

Market trends highlight the growing demand for flexible financing options. Structures like A/B loans, mezzanine debt, and senior-subordinate notes allow for tailored risk management and control. Additionally, clearly defined decision-making processes and intercreditor agreements with negotiated cure periods help safeguard investments during financial challenges.

With commercial mortgage borrowings expected to hit $645 billion in 2023 and $1.1 trillion in debt maturing in 2024, the need for tailored financing solutions is only increasing. Fixed interest rates can shield against cash flow issues, while committed facilities provide the flexibility to draw funds as needed.

For those exploring real estate syndications, platforms like Lofty make it easier to invest through fractional ownership, requiring neither large down payments nor deep real estate expertise. A solid understanding of debt structures — from payment waterfalls to default provisions — can help investors make smarter decisions and protect their capital.

Every detail, from consent terms to payment waterfalls, contributes to creating strong and adaptable syndication deals. Whether you’re structuring a financing package or evaluating an investment, customized debt terms are essential for balancing risk, returns, and operational flexibility.

FAQs

Which loan terms should be customized first in a syndication?

When setting up a loan syndication, the initial terms that usually get tailored include interest rates, repayment schedules, and covenants. These elements are hammered out during the structuring phase to strike a balance between the borrower’s needs and the lenders’ expectations. This process helps establish a framework that aligns with the syndication’s objectives while allowing some flexibility.

How do consent thresholds stop one lender from blocking changes?

Consent thresholds are designed to prevent a single lender from blocking changes to a loan agreement. Instead, they require approval from a specified majority or supermajority of lenders before amendments can be made. This approach ensures no single lender has unilateral veto power, encouraging balanced and flexible decision-making within syndication structures.

When should you use A/B loans vs mezzanine debt vs senior-subordinate notes?

A/B loans are a mix of senior (A) and subordinate (B) loans, making them a good option for projects that require multiple layers of financing. These loans establish a clear repayment hierarchy, with the senior portion being repaid first.

Mezzanine debt steps in as a bridge between senior debt and equity. It’s a way to secure extra capital for projects that come with higher risks and potentially higher returns. The best part? It doesn’t dilute ownership, which can be a significant advantage for stakeholders.

Senior-subordinate notes organize debt into multiple tiers. Senior notes take precedence when it comes to repayment, while subordinate notes are paid afterward. This setup is often used in complex real estate deals or securitization arrangements.

The right choice depends on your project’s risk tolerance, repayment priorities, and need for financial flexibility.

Jerry Chu