'/%3e%3cpath%20d='M110.5%2074.84L61.56%20113.3V150.04H0V87.4L110.5%200V74.84Z'%20fill='url(%23paint1_linear_1102_1766)'/%3e%3cpath%20d='M159.44%20150.04L159.44%20205.81H159.2L110.5%20166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57L159.44%20150.04Z'%20fill='url(%23paint2_linear_1102_1766)'/%3e%3cpath%20d='M110.5%20110.57V166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57Z'%20fill='url(%23paint3_linear_1102_1766)'/%3e%3cpath%20d='M159.44%20206H61.5601L61.8001%20205.81L110.5%20166.53L159.2%20205.81L159.44%20206Z'%20fill='url(%23paint4_linear_1102_1766)'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1102_1766'%20x1='166'%20y1='-19.908'%20x2='145.641'%20y2='227.731'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.723958'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_1102_1766'%20x1='64'%20y1='15.7891'%20x2='172.309'%20y2='257.652'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%239383FF'/%3e%3cstop%20offset='0.75'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_1102_1766'%20x1='171.462'%20y1='36.6188'%20x2='8.598'%20y2='270.272'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.229167'%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.994792'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_1102_1766'%20x1='55.7219'%20y1='-31.3876'%20x2='76.8187'%20y2='349.172'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.307292'%20stop-color='%239383FF'/%3e%3cstop%20offset='0.854167'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_1102_1766'%20x1='110'%20y1='271'%20x2='76.5255'%20y2='202.314'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.90625'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

'/%3e%3cpath%20d='M110.5%2074.84L61.56%20113.3V150.04H0V87.4L110.5%200V74.84Z'%20fill='url(%23paint1_linear_1102_1752)'/%3e%3cpath%20d='M159.44%20150.04L159.44%20205.81H159.2L110.5%20166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57L159.44%20150.04Z'%20fill='url(%23paint2_linear_1102_1752)'/%3e%3cpath%20d='M110.5%20110.57V166.53L61.8001%20205.81H61.5601L61.56%20150.04L110.5%20110.57Z'%20fill='url(%23paint3_linear_1102_1752)'/%3e%3cpath%20d='M159.44%20206H61.5601L61.8001%20205.81L110.5%20166.53L159.2%20205.81L159.44%20206Z'%20fill='url(%23paint4_linear_1102_1752)'/%3e%3cdefs%3e%3clinearGradient%20id='paint0_linear_1102_1752'%20x1='166'%20y1='-19.908'%20x2='145.641'%20y2='227.731'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.723958'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint1_linear_1102_1752'%20x1='64'%20y1='15.7891'%20x2='172.309'%20y2='257.652'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%239383FF'/%3e%3cstop%20offset='0.75'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint2_linear_1102_1752'%20x1='171.462'%20y1='36.6188'%20x2='8.598'%20y2='270.272'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.229167'%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.994792'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint3_linear_1102_1752'%20x1='55.7219'%20y1='-31.3876'%20x2='76.8187'%20y2='349.172'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20offset='0.307292'%20stop-color='%239383FF'/%3e%3cstop%20offset='0.854167'%20stop-color='%234D3FED'/%3e%3c/linearGradient%3e%3clinearGradient%20id='paint4_linear_1102_1752'%20x1='110'%20y1='271'%20x2='76.5255'%20y2='202.314'%20gradientUnits='userSpaceOnUse'%3e%3cstop%20stop-color='%23B5AAFF'/%3e%3cstop%20offset='0.90625'%20stop-color='%238977FF'/%3e%3c/linearGradient%3e%3c/defs%3e%3c/svg%3e)

Checklist for Fractional Real Estate Retirement Planning

Jerry Chu

Fractional real estate can be a smart way to generate passive income during retirement without the hassle of managing properties yourself. Instead of buying entire properties, you invest in shares of real estate projects, earning a portion of rental income and appreciation. This strategy allows you to diversify your portfolio across multiple property types and locations, starting with as little as $50.

Here’s the basic process:

- Review finances: Understand your income, expenses, and how much you can safely invest to build a sustainable portfolio.

- Set goals: Decide if you want steady income, long-term growth, or both.

- Choose a platform: Research fractional real estate platforms for fees, transparency, and liquidity options.

- Diversify investments: Spread your money across property types and markets to reduce risk.

- Understand taxes: Learn how rental income and capital gains are taxed, and take advantage of deductions.

- Monitor performance: Track returns and adjust investments as needed.

Fractional real estate offers a way to access high-value properties without large upfront costs, but it’s important to plan carefully, understand the risks, and regularly review your portfolio.

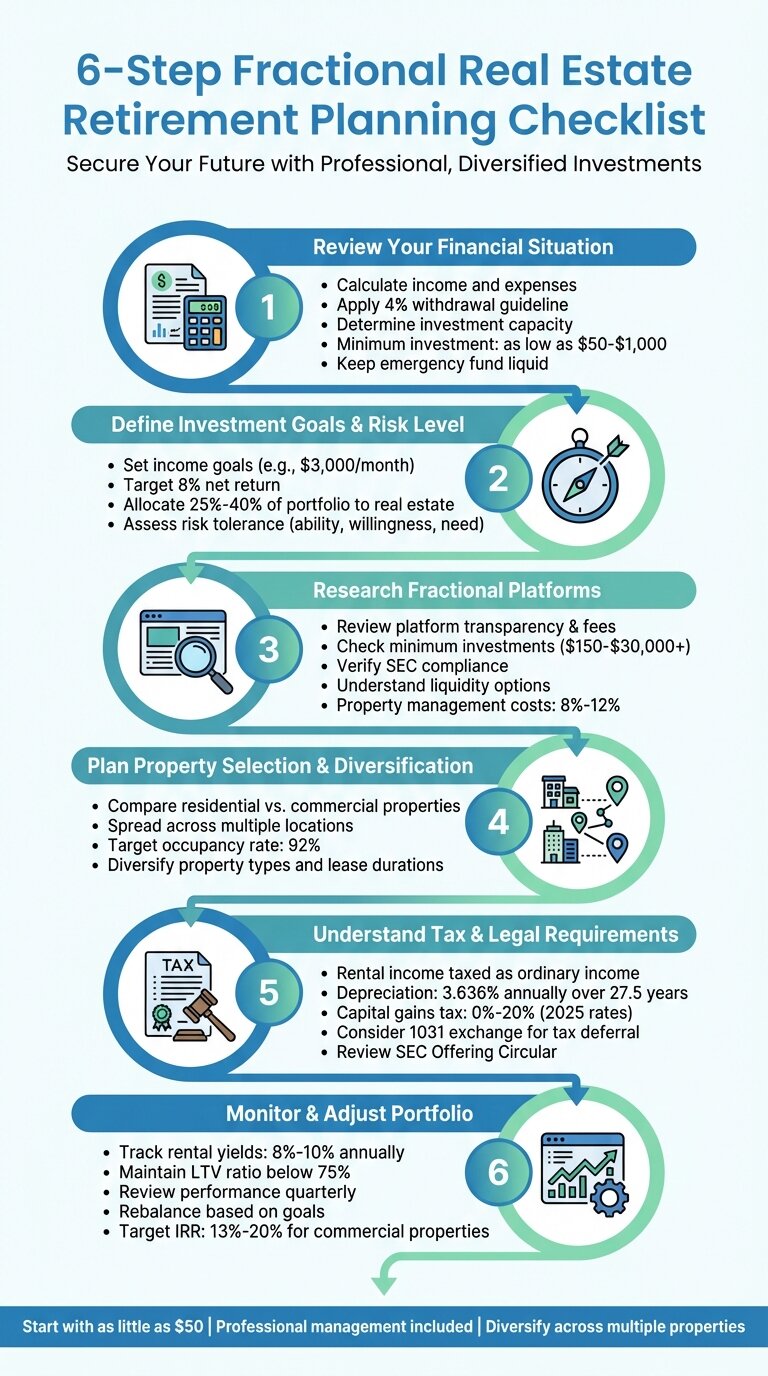

Step 1: Review Your Financial Situation

Before diving into real estate investments, take a close look at your financial picture. Understanding your income, expenses, and how much you can safely invest is critical.

Calculate Your Income and Expenses

Start by listing all your income sources. This includes steady streams like Social Security or pensions, as well as variable sources such as IRA or 401(k) withdrawals, dividends, or rental income. Forget the outdated “80% rule” that claims retirees need 80% of their pre-retirement income , it’s not one-size-fits-all.

Next, assess your expenses. Cover the essentials like housing (mortgage or rent, property taxes, insurance), utilities, and groceries. Don’t forget retirement-specific costs like healthcare, travel, hobbies, and social events.

“Start researching, visualizing retirement, having conversations, and asking questions.” , Alexa Kane, CFP®, CDFA®, Pearl Planning

To ensure your financial plan is sustainable, calculate your annual withdrawal rate relative to your portfolio value. Many experts recommend the “4% guideline”, which involves withdrawing 4% in the first year and adjusting for inflation afterward. Also, categorize your assets into tax-deferred, taxable, and Roth accounts to better understand their impact on your net income.

Once you’ve established a clear financial baseline, you’ll be ready to determine how much you can safely invest in fractional real estate.

Determine How Much You Can Invest

Figure out how much you can allocate to real estate without compromising your liquidity. Real estate investments are less liquid than stocks or bonds, so avoid tying up cash you might need in the next 5 to 10 years.

“Decisions about how to handle real estate investments prior to retirement are extremely individual, but in general, investors need to consider what their cash flow will be like in retirement.” , Dean Deutz, Private Wealth Consultant, RBC Wealth Management–U.S.

If you already own real estate, adjust your fractional investment to maintain a balanced portfolio. Traditional real estate investments often require a 20% down payment and another 2% to 5% for closing costs. With fractional real estate, however, you can start with as little as $1,000. Keep in mind that professional property management typically costs 8% to 12% of rental income, which can affect your returns.

To protect yourself during market downturns, maintain an emergency fund in liquid assets like money market accounts or certificates of deposit.

Once you’ve determined your investment capacity, focus on setting clear financial goals for your real estate portfolio.

Set Clear Financial Goals

Define a monthly income goal, such as $3,000 after retirement benefits, to guide your investment decisions. This target will help you calculate how many fractional shares or properties you need to reach financial independence.

Aim for an 8% net return to account for the risks and illiquidity of real estate investments. Be realistic , subtract 10% for property management fees and another 10% for potential vacancies. Use a conservative occupancy rate of 92%, even in high-demand areas.

“Income property can be an important bridge to retirement for those without quite enough to retire in the traditional sense.” , Jeff Camarda, CEO, Camarda Wealth Advisory Group

Decide how much of your total net worth to allocate to real estate. A common range is 25% to 40%, including your primary residence. Also, aim for your investment income to grow over time. Rising property values and rents typically keep pace with inflation, helping you maintain your purchasing power.

Step 2: Define Your Investment Goals and Risk Level

After understanding your financial capacity, the next step is to pinpoint what you want to achieve with fractional real estate investments. Your goals will guide the types of properties you choose and how you build your portfolio.

Decide What You Want to Achieve

Start by defining your primary objective. Are you aiming for consistent monthly income, long-term property value growth over 5 to 10 years, or a hedge against inflation? Real estate often tracks with the Consumer Price Index, making it a potential inflation buffer.

If passive income is your goal, look for properties with experienced professional management. For example, in late 2024, Realbricks , a fractional investment platform , offered investors a quarterly dividend of 2.25%, equating to an annual return of approximately 9.4%. On the other hand, if you’re focused on property appreciation, target high-growth areas or emerging markets where values are expected to rise.

“You want to earn at least 8% from the capital invested in the rental, net of all expenses.” , John Graves, Managing Principal, Retirement Journal

Diversifying your portfolio is another key strategy. Spread your investments across different property types and locations to reduce the impact of market fluctuations. If you anticipate needing access to your funds sooner rather than later, consider platforms that offer secondary resale markets for liquidity.

Once you’ve set your objectives, it’s time to evaluate your comfort level with risk.

Understand Your Risk Tolerance

Risk tolerance measures how much financial loss you can handle during downturns. For retirees, this assessment includes three factors: your ability (financial capacity to absorb losses), your willingness (emotional comfort with market volatility), and your need (the returns required to meet your goals).

Because retirees typically no longer have income from work, their ability to take risks is generally lower than younger investors. Factors like your investment time horizon, liquidity needs, and backup plans if things don’t go as expected are crucial. In fractional real estate, you should also consider risks related to asset quality, platform management, and liquidity.

A practical way to assess your comfort with risk is the “sleep test.” Imagine a bear market scenario and calculate how much you could lose in dollar terms. Would you stick to your plan, or would the losses keep you up at night? Before investing, ensure the platform you choose complies with SEC regulations, provides audited financials, and uses third-party fund custodians. Additionally, check whether the platform offers a secondary market or quarterly valuation windows to manage liquidity risks.

“Risk doesn’t disappear when you fractionalize an asset; it just gets distributed.” , Raveum Insights

Set Your Real Estate Allocation Target

Aligning your real estate investments with your risk tolerance and financial goals is essential. Based on your objectives, decide how much of your overall portfolio should go into real estate to balance income and growth.

Experts suggest allocating 25%–40% of your portfolio to real estate for a mix of growth, income, and diversification. High-net-worth investors often keep around 27% of their portfolio in real estate. If liquidity is a priority, consider allocating 5%–15% to REITs or similar liquid fractional platforms.

To evaluate your current real estate exposure, divide the total value of your real estate holdings , including home equity , by your total net worth. Many Americans have between 45% and 70% of their net worth tied up in their primary residence, which can create liquidity challenges in retirement. If over 40% of your net worth is tied to your home, it may be wise to shift some investments into more liquid assets or fractional real estate to ensure you have accessible cash.

“As you near retirement, you’ll have more experience, but you’ll also have less physical potential and less interest in actively managing your properties. It’s a great time to… shift your focus to REITs [or fractional platforms] to make your real estate more passive.” , Deanna Ritchie, Managing Editor, Due

Tailor your allocation to your goals. If you’re still building wealth, focus on properties with high appreciation potential. But if you need steady monthly cash flow for living expenses, prioritize high-yield rental fractions.

Step 3: Research Fractional Real Estate Platforms

Once you’ve figured out how much of your portfolio you want to allocate to fractional real estate, the next step is finding the right platform to bring your strategy to life. Not all fractional real estate marketplaces are the same, and picking the wrong one could mean dealing with high fees, limited liquidity, or compliance headaches.

Review Platform Features and Transparency

Start by digging into how a platform evaluates properties and manages investments. Look for detailed property data , like location, rental history, and condition reports. A trustworthy platform will also clearly lay out its fee structure, including acquisition fees, management costs, and any transaction charges. For retirees aiming for steady passive income, professional property management is key. These services typically cost between 8% and 12%.

Transparency is another must-have. The platform should provide regular financial updates, audited statements, third-party property appraisals, clear SPV (special purpose vehicle) documentation, and compliance with SEC regulations. Platforms such as Lofty stand out by offering daily rental income distributions and real-time property performance tracking, so you’re not left waiting for quarterly reports.

“Clients often want to wait until they are 80 to sell their property, so it works well for them to hire someone to manage their properties, or to own property that essentially runs itself.” , Dean Deutz, Private Wealth Consultant, RBC Wealth Management

Lastly, check the platform’s minimum investment requirements to see how easily you can diversify your portfolio.

Check Minimum Investment Amounts

Minimum investment thresholds vary widely, and they can have a big impact on how you spread your risk. Some tokenized platforms or publicly traded REITs let you start with as little as $150 to $500, while premium commercial properties might require $30,000 or more. For retirees on a fixed budget, lower minimums can make it easier to distribute investments across multiple properties and markets.

If you’re using a self-directed IRA (SDIRA), it’s worth noting that the IRS requires all related expenses , like closing costs, taxes, insurance, and maintenance , to be paid directly from your retirement account. Take the time to calculate the total cost of ownership to ensure your account has enough liquidity to cover ongoing expenses without breaking IRS rules. Also, remember that setting up and funding an SDIRA can take two to four weeks, so plan ahead.

Some platforms may also require you to qualify as an “Accredited Investor” to access high-value commercial properties. This means meeting specific income or net worth criteria. Confirm these requirements upfront to avoid wasting time on platforms you can’t use.

Understand Liquidity and Exit Options

Once you’ve reviewed the platform’s features and costs, focus on how easily you can sell or adjust your investment. Liquidity is often a challenge in fractional real estate. Unlike publicly traded REITs, most platforms have limited exit options. Some offer secondary markets where you can sell your shares to other investors, while others provide quarterly valuation windows or redemption programs, often with restrictions or fees.

Before committing, find out how long it typically takes to liquidate your investment and whether there are penalties for early withdrawals. If you think you’ll need access to your funds in a few years, look for platforms with active secondary markets or shorter holding periods. For instance, Lofty allows investors to buy and sell real estate fractions instantly, giving more flexibility compared to traditional syndications that might lock up your money for five to ten years.

“Decisions about how to handle real estate investments prior to retirement are extremely individual, but in general, investors need to consider what their cash flow will be like in retirement.” , Dean Deutz, Private Wealth Consultant, RBC Wealth Management

Keep in mind that rental yields for fractional real estate investments typically range between 8% and 10% annually.

Step 4: Plan Your Property Selection and Diversification

Once you’ve completed your platform research, it’s time to plan your property investments thoughtfully. Choosing the right properties and diversifying your portfolio are key steps to managing risk effectively. Avoid putting all your money into a single property or region , spreading your investments helps protect against market fluctuations.

Compare Different Property Types

Not all property types perform the same way during economic shifts. Residential properties , like single-family homes and apartments , are often easier to understand and tend to have consistent demand. However, their performance can be influenced by local job markets. On the other hand, commercial properties , such as warehouses, office buildings, and retail spaces , often feature longer lease terms and tenants with strong financial backing, offering more stability. For instance, U.S. net lease assets delivered an 8.1% return in 2023.

When evaluating properties, focus on factors like tenant creditworthiness, lease duration, and occupancy rates. Stable U.S. commercial properties often maintain a median debt ratio below 55% and have tenant retention rates exceeding 80%. If you’re seeking inflation-resistant options, consider commercial properties in high-demand metro areas with built-in rent escalations.

“The best investors don’t chase returns, they interrogate risk.” , Raveum Insights

Instead of simply chasing high yields, prioritize risk metrics like debt-to-value ratios and coverage ratios. Collect essential data such as net operating income (NOI), cap rates, and maintenance costs before making any investment decisions. These insights help you strike the right balance between risk and return.

Spread Investments Across Locations and Markets

Diversifying geographically is another way to protect your portfolio. Localized economic downturns, natural disasters, or policy changes can severely impact specific regions. To mitigate this, consider spreading your investments across multiple areas. For example, combining properties in states like Texas, Ohio, Florida, and Washington exposes you to different economic drivers and housing markets.

“Putting all your eggs in one basket is the fastest way to lose all your eggs.” , Paul Esajian, Co-Founder, FortuneBuilders

Fractional ownership makes geographic diversification much more accessible. Instead of needing substantial capital to purchase multiple properties outright, platforms like Lofty let you invest in fractions of properties across the U.S., allowing you to balance exposure between emerging and established markets.

You can also diversify by varying lease durations and investment timing. Combining short-term vacation rentals with long-term net lease properties can help maintain a steady income stream while reducing the impact of poor market timing. This strategy ensures cash flow regardless of which sector is performing well at any given moment.

Once you’ve built a diversified portfolio, the next step is to familiarize yourself with the tax and legal requirements of your investments.

Step 5: Understand Tax and Legal Requirements

After diversifying your portfolio, it’s time to tackle the tax and legal aspects of your retirement investments. Overlooking these details can lead to unexpected tax bills or missed deductions, which no retiree wants.

Learn About Rental Income and Capital Gains Taxes

Income from fractional property rentals is taxed as ordinary income. However, you can deduct certain expenses like mortgage interest, property taxes, insurance, maintenance, and management fees. Additionally, you can depreciate the building (not the land) over 27.5 years , approximately 3.636% annually , to reduce your taxable income. For 2025, single filers earning between $48,475 and $103,350 will fall into the 22% tax bracket for that portion of income.

If you’re using a platform like Lofty, ensure they provide a detailed breakdown of your share of income and expenses. This is crucial because you’re responsible for reporting your specific ownership percentage.

Be aware of the Net Investment Income Tax (NIIT), which adds an extra 3.8% tax if your Modified Adjusted Gross Income exceeds $200,000 (single filers) or $250,000 (married filing jointly). Rental income is typically classified as passive, meaning losses can only offset other passive income unless you actively manage the property and earn less than $100,000 per year.

When selling a fractional property, you’ll encounter capital gains tax on the appreciation and depreciation recapture , the latter taxed at up to 25% on the deductions you’ve claimed. Long-term capital gains tax rates for 2025 range from 0% to 20%, depending on your income. To defer these taxes, consider a 1031 exchange, which allows you to reinvest proceeds into another “like-kind” property without immediate taxation. Keep detailed records of all purchase costs, legal fees, and capital improvements, as these can increase your property’s basis and reduce your taxable gain.

While understanding taxes is essential, legal compliance is just as critical for protecting your investment.

Verify Legal Compliance and Property Vetting

Before investing, review key legal documents such as the SEC-required Offering Circular, Operating Agreement, and Subscription Agreement. These documents outline financial risks and your responsibilities as an investor.

“Compliance requires thorough financial and risk disclosures which provide investors with detailed information about the prospective investment, which enhances transparency and investor protection.” , Realbricks

When it’s time to file taxes, you’ll need to submit Schedule E for rental income and losses, Form 4562 for depreciation, and Form 1098 for mortgage interest exceeding $600. If you have rental losses, report them using Form 8582. Since platforms don’t provide tax advice, consulting a licensed tax advisor is a smart move to ensure you meet all IRS requirements.

Make sure to also review the platform’s Terms of Service and confirm that all parties involved have valid Taxpayer Identification Numbers (TINs). The IRS won’t process certain forms without this information. By staying on top of these legal safeguards, you’ll protect your investment and be well-prepared when tax season rolls around.

With taxes and legal compliance sorted, the next step is to actively monitor and adjust your portfolio as needed.

Step 6: Monitor and Adjust Your Portfolio

Keeping a close eye on your fractional real estate investments is essential to ensure your retirement plan stays on track. With these investments, you’ll need to monitor two main types of returns: the regular cash flow from rental income and the long-term value growth as property prices appreciate over time. Unlike traditional stocks, real estate performance hinges on both day-to-day operational metrics (how well the property functions) and investor-level returns (how effectively your capital is performing).

Track Your Investment Performance

To stay organized, align your financial records with IRS Schedule E by using a Chart of Accounts. Consistency in tracking methods across all your investments is key , it ensures you’re making fair comparisons.

“Tracking property performance begins with keeping track of income and expenses.” , Stessa

While a spreadsheet might work for a handful of properties, it can quickly become overwhelming and error-prone as your portfolio grows. That’s where rental property management software like Stessa or Buildium comes in handy. These tools can automate tasks like downloading bank transactions, updating mortgage balances in real time, and calculating advanced metrics such as Internal Rate of Return (IRR) and Cash-on-Cash Return.

Keep an eye on your Loan-to-Value (LTV) ratio, which should ideally stay below 75% to avoid unnecessary financial risks. If your LTV exceeds 75%, it could indicate higher exposure to debt. Platforms like Lofty can simplify this process by providing dashboards that display your income, expenses, and property valuations, all in one place.

As your portfolio grows to include 15–20 passive investments, managing everything on your own may become impractical. At this stage, consider hiring professional help or using advanced reporting tools to streamline your monthly reviews. Also, make it a habit to maintain digital copies of essential documents , such as rent receipts, vendor invoices, and tax forms , to ensure your bookkeeping is accurate and well-supported.

These tracking efforts will provide the insights you need to make informed adjustments to your portfolio.

Review Goals and Adjust Investments as Needed

Retirement goals and market conditions evolve over time, so regularly reviewing your portfolio is critical. By staying proactive, you can ensure your investments continue to align with your retirement objectives, even as circumstances change. For example, compare the current price of your property tokens to the fair market value (FMV) shown on your platform dashboard. If a property’s value rises significantly , say, more than 20% above FMV , it might be a good opportunity to sell those tokens, lock in the gains, and reinvest in undervalued properties.

Pay attention to the average yield of each property as well. If steady income is your priority, focus on properties with reliable yields and consider exiting investments with declining or unstable performance.

Most platforms offer secondary marketplaces where you can rebalance or exit positions. Keep in mind that some transactions may involve stablecoins like USDC, so plan how you’ll convert these digital assets back to USD when needed. Striking a balance between high-yield properties for immediate income and undervalued properties for long-term growth can help you maintain a well-rounded portfolio.

Also, monitor how responsive your investment sponsors are, especially during challenging times like paused distributions or capital calls. Quick and clear communication is a strong indicator of a reliable operator. If certain markets or property types are consistently underperforming, consider reallocating funds to areas with better potential.

Since fractional platforms typically don’t provide personalized advice, consult licensed investment and tax advisors before making major changes to your portfolio. Their expertise can help you navigate complex decisions and ensure your strategy remains sound.

Conclusion

This checklist provides a roadmap to create a balanced and diversified retirement portfolio using fractional real estate investments. It’s a way to secure steady passive income while leaving the day-to-day management to professionals. Each step highlights how these investments can align with your retirement objectives.

With fractional real estate, you can start investing with as little as $50 to $100, opening the door to high-value properties while spreading out risk. This strategy enables diversification across multiple assets, reducing the impact of any single property’s performance. Plus, professional management companies take care of the operational headaches , like maintenance, repairs, and tenant concerns , so you can focus on enjoying rental income without the stress.

“Fractional ownership is a real estate investing strategy involving multiple investors who own pieces of a single property. By pooling their resources, investors can get an ownership stake in properties they may not otherwise be able to afford.” , Robin Hartill, CFP®, Yahoo Personal Finance

The combination of monthly rental income and long-term property appreciation can significantly enhance your retirement savings. For instance, fractional commercial real estate often delivers an IRR of 13%–20%. Platforms like Lofty make it simple to track your investments and offer liquidity options. By regularly evaluating your financial situation, setting clear goals, and choosing the right platform, you can adjust your portfolio as needed to stay on course.

That said, real estate investing , fractional or otherwise , requires consistent oversight. Regularly monitoring your investments, diversifying geographically, and rebalancing your portfolio are essential steps to ensure long-term success. These practices will help you adapt to market changes and evolving personal needs. With careful planning and discipline, fractional real estate can become a key pillar of your retirement income strategy.

FAQs

How much should I invest in fractional real estate for retirement?

The amount you should invest in fractional real estate for retirement hinges on factors like your financial goals, risk appetite, and how much capital you have to work with. Platforms such as Lofty make this option more accessible, allowing you to start with investments as low as $50. Adding fractional real estate to your retirement portfolio can help spread out risk and create passive income, making it an effective component of your broader retirement plan.

How do I get my money out if I need cash later?

You can tap into your funds by selling part of your equity through Lofty’s marketplace, which provides competitive valuations and keeps fees low. Other routes include selling directly to co-owners, collaborating with real estate brokers, arranging buyout agreements, or utilizing secondary market exchanges. Pick the option that aligns best with your goals and circumstances.

Can I hold fractional real estate in an IRA, and what rules apply?

Yes, it’s possible to hold fractional real estate in an IRA, but it must be done through a self-directed IRA (SDIRA). However, the IRS enforces strict rules for this arrangement. For instance, you’re prohibited from using the property personally, engaging in transactions with disqualified persons, or handling income and expenses outside of the IRA. All financial activity related to the investment must flow directly through the IRA to stay compliant and avoid penalties.

Jerry Chu