REITs vs. Direct Real Estate: Risk Comparison

Jerry Chu

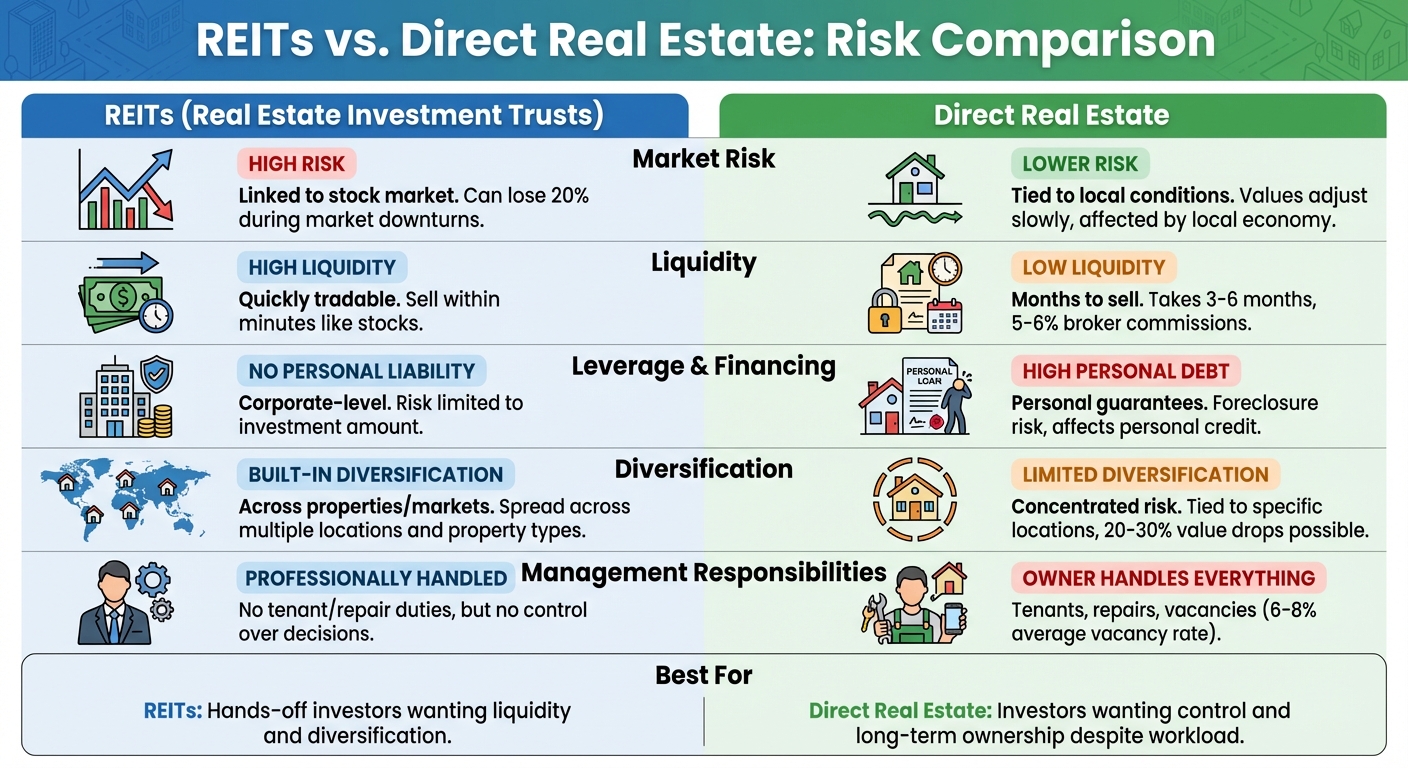

When deciding between REITs (Real Estate Investment Trusts) and direct real estate ownership, understanding the risks is crucial. REITs offer liquidity, diversification, and professional management but are tied to stock market volatility and limited control. Direct real estate provides hands-on control, potential tax advantages, and leverage opportunities but comes with high responsibility, illiquidity, and localized risks.

Key Takeaways:

- REITs: Easy to buy/sell, diversified, no personal debt, but subject to stock market fluctuations and management decisions.

- Direct Real Estate: Greater control, potential for higher returns via leverage, but has high transaction costs, tenant challenges, and concentrated risk.

Quick Comparison:

| Risk Aspect | REITs | Direct Real Estate |

|---|---|---|

| Market Volatility | High (linked to stock market) | Lower (tied to local conditions) |

| Liquidity | High (quickly tradable) | Low (months to sell property) |

| Leverage | Corporate-level, no personal liability | High, personal debt amplifies risks |

| Diversification | Built-in across properties/markets | Limited, tied to specific locations |

| Management | Professionally handled | Owner handles tenants, repairs, etc. |

If you prefer hands-off investing and liquidity, REITs may suit you. If you value control and long-term property ownership despite the workload, direct real estate might be better. A mix of both could balance risks and rewards.

REITs vs Direct Real Estate Investment Risk Comparison Chart

REITs vs Direct Real Estate Investment

Main Risk Categories: REITs vs. Direct Real Estate

When investing in real estate, understanding how different risks affect your portfolio is critical. Real estate investment trusts (REITs) and direct property ownership both expose you to real estate, but the types of risks - and how they influence returns - are quite distinct. The three main risk categories to consider are market risk, liquidity risk, and leverage and financing risk. These factors shape your returns, your ability to sell investments, and your exposure to debt-related challenges. Let’s break down how these risks uniquely impact REITs and direct real estate investments.

Market Risk

Market risk refers to how broader economic factors influence the value of your investment. For REITs, this risk is closely tied to the stock market. Since public REITs trade on U.S. stock exchanges, their share prices fluctuate daily based on market sentiment. For example, a diversified U.S. equity REIT ETF could lose 20% during a market downturn, even if the underlying properties remain stable and tenants continue to pay rent. Factors like Federal Reserve interest rate hikes, recession fears, or general market sell-offs can quickly impact REIT prices.

In contrast, direct real estate investments are more influenced by local market conditions. The value of a rental property depends on factors like job growth in your city, neighborhood trends, and the local supply and demand for housing. Unlike REITs, property values don’t react to daily stock market swings. However, local disruptions - such as a major employer leaving town or rising crime rates - can significantly hurt a property’s value. A diversified REIT portfolio might not feel the impact of these localized issues, but an individual property could take a big hit. Essentially, REITs are more exposed to stock market volatility, while direct real estate is driven by local economic and social factors. Understanding these differences helps you choose an investment that matches your risk tolerance and goals.

Liquidity Risk

Liquidity risk measures how easily you can convert your investment into cash. REITs are known for their high liquidity. You can buy or sell shares in a REIT within minutes through a brokerage account, just like trading stocks. This makes REITs a good option if you need access to your money in the short term or want the flexibility to rebalance your portfolio quickly.

Direct real estate, on the other hand, is much less liquid. Selling a property can take weeks or even months and involves a lengthy process that includes marketing, inspections, appraisals, negotiations, and closing. On top of that, residential property sales often incur 5%–6% broker commissions and additional closing costs. In a slow market, you might have to lower your asking price to attract buyers. If you suddenly need cash - due to an emergency or unexpected expense - owning a physical property offers little immediate help. While fractional ownership platforms can speed up transactions, they still carry market and tenant risks. This stark difference in liquidity can significantly affect your ability to respond to financial needs or seize new investment opportunities.

Leverage and Financing Risk

Debt plays a major role in real estate investing, and leverage and financing risk examines how borrowing money can amplify both gains and losses. For direct property ownership, most investors rely on mortgage financing. This typically involves a down payment and personal guarantees, meaning your lender can pursue your personal assets if the property underperforms and you default. During economic downturns, if rental income doesn’t cover your mortgage payments or you can’t refinance when your loan matures - especially in a rising interest rate environment - you risk foreclosure and damage to your personal credit. For example, a landlord with a 75% loan-to-value mortgage on a $300,000 rental could lose the property and their equity if vacancies increase and cash flow dries up.

REITs, however, handle debt differently. They use leverage at the corporate or portfolio level, meaning individual shareholders are not personally liable. Your risk is limited to the money you’ve invested in REIT shares. REITs can refinance through public debt and equity markets, but rising interest rates can still reduce profit margins, lower funds available for dividends, and push share prices down. A diversified REIT with debt spread across multiple properties is generally better equipped to weather short-term cash flow issues than a highly leveraged individual landlord. That said, rising borrowing costs can still hurt REIT performance and reduce income distributions. Deciding between personal liability and corporate-level debt is an important step in determining which investment structure aligns with your financial comfort zone.

REIT Risk Profile

REITs come with their own set of challenges, particularly when it comes to market volatility, income reliability, and management practices. Unlike owning physical property, REITs are traded on public stock exchanges, which exposes them to daily price fluctuations driven by market sentiment, interest rate changes, and investor behavior. These swings often don't reflect the actual performance of the underlying real estate. Let’s break down the key risks: volatility, income vulnerabilities, and management oversight.

Volatility and Stock Market Correlation

Publicly traded REITs often mirror the broader stock market in the short term. For instance, when the Federal Reserve raises interest rates or economic uncertainty grows, REIT share prices tend to drop alongside major indices like the S&P 500 - even if tenants are still paying rent and property values remain solid. During turbulent times, REIT prices can fall by as much as 20–30%, while private real estate valuations adjust more slowly and with less frequent changes. This means REIT investors must be prepared for rapid price swings, even though real estate itself is a slower-moving asset class. Over the long term, however, REIT performance tends to align more closely with the actual fundamentals of the properties they own.

Income and Dividend Risks

One of the defining features of REITs is their requirement to distribute at least 90% of taxable income as dividends. While this often results in high yields - sometimes exceeding 10% - it also leaves REITs with limited ability to retain earnings or build cash reserves. This creates vulnerabilities during economic downturns. For example, tenants may default, renegotiate leases, or close their businesses, which reduces a REIT’s operating income and puts pressure on dividend payments. In tough times, some REITs have cut dividends by 30–50% or more or even issued partial stock dividends to conserve cash. A high dividend yield can also serve as a warning sign, suggesting market concerns about potential cuts or financial stress in the portfolio.

The stability of a REIT’s cash flow depends heavily on occupancy rates and lease agreements. REITs with long-term leases, like triple-net leases, often experience steadier income but still face risks like inflation or challenges when leases expire. On the other hand, sectors such as hotels or self-storage, which adjust pricing more frequently, are more sensitive to economic cycles. Additionally, sector concentration can heighten risks. For example, a REIT heavily invested in office spaces may struggle with the rise of remote work, while one focused on retail could be impacted by shifting consumer habits. Tenant concentration is another factor - if a few tenants make up a large portion of rental income, losing just one major tenant could significantly affect cash flow.

Management and Governance Risks

Investing in a REIT means placing trust in its management team, as investors have no direct control over property decisions. Unlike owning real estate directly, where you can set rents, plan renovations, or decide when to sell, REIT investors rely entirely on management to make these calls. The success of a REIT depends on the team’s ability to acquire properties wisely, manage them efficiently, allocate capital effectively, and control risks. Poor decisions, such as overpaying for assets or relying too heavily on debt, can erode shareholder value and hurt long-term returns.

Additionally, fee structures, related-party transactions, and limited shareholder rights can sometimes lead to misaligned incentives or reduced accountability. In challenging markets, management might issue new shares at low prices, cut dividends, or sell properties at a discount to shore up the balance sheet - moves that can harm investor returns while leaving shareholders with few options for recourse. Before investing in a REIT, it’s essential to evaluate the management team’s track record, fee policies, and governance practices to understand the risks involved fully.

sbb-itb-a24235f

Direct Real Estate Risk Profile

Owning property directly gives you complete control, but it also comes with hefty responsibilities and risks. Unlike REITs, where professionals handle the daily grind, direct ownership puts you in charge of everything - finding tenants, managing repairs, and dealing with market fluctuations. Let’s break down how tenant challenges, local market dynamics, and costly sales processes shape the risks of direct real estate investments.

Tenant and Operating Risks

Managing tenants and maintaining property is no small task. Tenant turnover can leave your property sitting empty for weeks or even months, especially during tough economic times when finding qualified renters is harder. On average, U.S. vacancy rates hover around 6–8%, but extended vacancies can slash annual income by as much as 10–20%. Late rent payments can throw off your cash flow, and evictions - costing anywhere from $3,500 to $10,000 in legal fees - can add months of lost rent to your financial headaches.

Then there are the repair costs, which can hit hard. A major plumbing issue, a broken HVAC system, or replacing a roof on a single-family home can easily set you back $10,000 to $50,000. For instance, HVAC repairs alone typically cost between $5,000 and $15,000, while damage from natural disasters can require immediate and expensive fixes. These unexpected expenses often mean dipping into personal savings or delaying other financial goals. On top of that, coordinating repairs, ensuring code compliance, and addressing tenant concerns can be a full-time job if you don’t hire professional management.

Concentration and Local Market Risks

Owning just one or a few properties naturally concentrates your risk. If the local economy takes a hit - maybe a major employer shuts down or nearby businesses close - your property’s value and rental demand could plummet by 20–30%. The 2008 financial crisis offers a stark example. Cities like Las Vegas and parts of Florida saw property values drop by 50–60% due to oversupply and foreclosures, leaving many owners stuck with negative equity and few options to recover. Unlike diversified investments spread across locations and property types, a single property in a struggling market can drag down your entire portfolio.

Liquidity and Transaction Costs

Selling a property isn’t quick or easy. Unlike REITs, which you can sell like stocks, unloading real estate can take months. On average, it takes 3–6 months to sell a property, and even longer in slow markets. During this time, you’re still on the hook for mortgage payments, taxes, and maintenance costs. Plus, finding a buyer, addressing inspection issues, or dealing with appraisal discrepancies can stretch the process further. If you’re in a hurry, you might have to sell for 10–20% below market value just to close the deal.

The costs of selling only add to the challenge. Transaction expenses typically run between 8–12% of the sale price. For example, selling a $400,000 property could cost you $32,000 to $48,000 in fees, which eats into your profits and makes quick exits far less practical than selling more liquid investments. Combined, these high costs and long timelines make direct real estate one of the least liquid investment options out there.

Side-by-Side Risk Comparison

Risk Comparison Table

Looking at the risks side-by-side, it's clear that REITs and direct real estate ownership come with their own unique challenges, especially when it comes to capital, time, and investor confidence.

| Risk Dimension | REITs | Direct Real Estate |

|---|---|---|

| Market Risk | High – Prone to stock market fluctuations and interest rate changes. | Lower short-term volatility, but property values can drop during local economic downturns. |

| Liquidity | High – Can be quickly bought or sold through a brokerage account. | Low – Selling property typically takes months and incurs high transaction costs. |

| Leverage Risk | Low – No personal debt involved, limiting both potential gains and losses. | High – Mortgages can amplify returns but also heighten risks, often requiring personal guarantees. |

| Diversification | Built-in – Investments cover multiple properties and locations. | Concentrated – Owning one or a few properties ties your portfolio to specific local market conditions. |

| Operating Responsibilities | None – Professionally managed. | High – Owners handle tenants, maintenance, vacancies, and compliance unless managers are hired. |

This comparison highlights the distinct risk factors, helping investors weigh liquidity, control, and management responsibilities.

What This Means for Investors

Understanding these differences lets investors make smarter choices about how to balance their portfolios. REITs are ideal for those who want a hands-off experience, offering diversified exposure, easy liquidity, and professional management. On the other hand, direct real estate ownership appeals to those who value control, potential tax perks, and the chance for long-term property appreciation - though it comes with the added workload of managing properties and navigating local market risks.

For those who want the best of both worlds, combining these strategies can create a balanced approach. REITs offer convenience and liquidity, while direct ownership provides control and leverage opportunities. Additionally, fractional real estate platforms like Lofty offer a hybrid solution. They allow you to invest in U.S. rental properties with relatively small initial investments, providing liquidity similar to REITs.

Choosing the Right Investment Based on Risk

Picking between REITs and direct real estate ownership isn’t about finding a “one-size-fits-all” solution - it’s about matching your investment choice to your risk tolerance. Each path comes with its own set of challenges. REITs offer diversification and professional management, sparing you from tenant troubles and property-specific issues. However, they’re tied to the ups and downs of the stock market. On the other hand, owning property directly gives you control and potential tax perks, but it comes with risks like illiquidity, concentration in a single asset, and surprise repair costs.

Ask yourself: Can you afford to lock up a large sum of money in one property for 5–10 years? How would you handle a 20–30% drop in your REIT’s value during a market downturn, even if the properties are still generating rental income? Are you ready to take on a mortgage that could affect your personal credit and assets during tough times? Many financial advisors suggest a balanced strategy - combining REITs for liquidity and diversification with direct or fractional real estate investments to gain control and tax benefits. This approach can help you align your investment choices with your financial goals and risk appetite.

Consider Fractional Real Estate Ownership

For those looking to invest in real estate without needing a large upfront capital, fractional ownership can be a practical option. Platforms like Lofty make it possible to invest in U.S. rental properties with minimal funds by purchasing fractional shares. Investors earn from both daily rental income and any appreciation in property value, and vote with their fellow co-owners on how to take care of tenant issues, repairs, and vacancies.

This setup minimizes some of the major risks associated with traditional real estate investing. You avoid personal guarantees and the leverage risks tied to mortgages. Plus, you can diversify across multiple properties and markets (Lofty, for instance, offers access to 150 properties in 40 different markets). It’s also more flexible than owning an entire property, making it a great option for those priced out of traditional real estate or looking to gradually build a diversified portfolio without adding extra workload.

Questions to Ask Yourself

Before diving into any investment, take a moment to reflect on these key questions. Your answers will help clarify which route aligns best with your goals, risk tolerance, and time commitment:

- Market volatility: Can you handle the daily fluctuations of REITs or the illiquidity of long-term property investments?

- Leverage: Are you okay with the risks tied to mortgages and personal guarantees, or would you prefer to avoid debt altogether?

- Operations: Do you have the time and willingness to manage tenants, repairs, and vacancies yourself - or would you rather have a hands-off investment?

Being honest about your comfort level with these factors will guide you toward the investment structure that best suits your financial situation and lifestyle.

FAQs

What are the key risks of investing in REITs versus owning real estate directly?

Investing in REITs and direct real estate presents different sets of risks and benefits. REITs, being traded on stock exchanges, are more exposed to market ups and downs and shifts in the broader economy. On the plus side, they’re highly liquid - you can buy or sell shares with ease. However, this liquidity also means their value can be swayed by market trends and investor sentiment.

Direct real estate ownership, by contrast, involves tangible properties that tend to show less short-term volatility. But this stability comes with property-specific challenges like upkeep costs, tenant-related issues, or downturns in the local market. Owning property also requires hands-on involvement or hiring a management team, which can add to both time and expenses.

Each approach has its perks, so it’s crucial to assess your financial goals and comfort with risk when choosing the right path for you.

How does market volatility impact REITs compared to direct real estate investments?

Market volatility tends to have a stronger impact on REITs because they’re traded on stock exchanges. This exposes their prices to daily market swings, which can result in more dramatic price changes. On the flip side, REITs offer higher liquidity, making it easier for investors to quickly buy or sell shares.

Direct real estate investments, however, are less affected by short-term market fluctuations. Property values tend to shift more slowly, driven by local factors like supply and demand or neighborhood trends. That said, selling or adjusting a direct real estate investment takes more time and effort, as it lacks the ease of liquidity that REITs provide.

How does liquidity differ between REITs and owning real estate directly?

REITs are known for their high liquidity because their shares are traded on stock exchanges. This means investors can buy or sell shares in just minutes, offering quick access to cash when needed. For those who value flexibility, this is a major advantage.

On the other hand, owning real estate directly is much less liquid. Selling a property can take weeks or even months due to the lengthy process of listing, finding a buyer, and completing the closing. As a result, direct ownership is generally more appropriate for long-term investments where immediate access to funds isn't a concern.

Related Blog Posts